Article Contents

Article ID: CM2621101024

Views: 28Evaluating the Effectiveness of Digital Bookkeeping Applications for the UK Small and Medium Enterprises: A User-Centric Approach with the Mediating Role of User Satisfaction

PDF

PDF

⬇ Downloads: 1

1Department of Business Administration, Jubail Industrial College, Jubail, Kingdom of Saudi Arabia

Received: 05 April, 2026

Accepted: 17 June, 2026

Revised: 08 June, 2026

Published: 06 July, 2026

Abstract:

Introduction: The research paper focuses on the perceived usefulness of digital bookkeeping applications in the context of the UK small and medium-sized enterprises (SMEs) and proposes a post-adoption, user-based follow-up to the Technology Acceptance Model (TAM), a model of technology adoption.

Methods: Perceived usefulness and the perceived ease of use were examined for their direct and mediated association via user satisfaction. To collect the quantitative data, an online survey of 500 SME finance officers, accountants, managers, and owners in different industries in the United Kingdom was conducted. Partial Least Squares Structural Equation Modelling (PLS-SEM) was used for measuring the constructs’ direct and mediating relationships.

Results: From the findings it was observed that the association was significant and positive between perceived usefulness and perceived effectiveness only and not between perceived ease of use and effectiveness. Both relationships are greatly mediated by user satisfaction, which means that experiential assessment is a crucial part of post-adoption technology evaluation.

Conclusion: The research adds to the literature as it offers a contextual expansion of TAM in regulated and digitally mature SME contexts and conceptualises perceived effectiveness as a post-adoption functioning outcome as opposed to being an adoption-related perception.

Keywords: Perceived usefulness, bookkeeping applications, effectiveness, user satisfaction, UK, SMEs.

1. INTRODUCTION

Over the last couple of years, the use of digital bookkeeping software has become increasingly common among small and medium-sized businesses (SMEs) to manage their financial data, fulfill tax obligations, and improve decision-making. Digital bookkeeping applications are software platforms (generally cloud-based or mobile) that automate the recording, classification, and reporting of business transactions, providing real-time visibility, automated reconciliation, and integrated reporting, compared to traditional manual methods and spreadsheets (Hussain, 2025; UNCDF, 2021). Among UK SMEs, including sole traders and limited companies, applications such as QuickBooks Online, Xero, Sage, Zoho Books, FreshBooks, and FreeAgent have become popular for simplifying bookkeeping, invoicing, bank integration, and VAT compliance under HMRC’s Making Tax Digital initiative (Adler, 2021). Such platforms have gained significance as SMEs seek regulatory reforms whereby they must utilise digital records and electronic submission of returns by using digital documents when providing tax returns (Mohamad & Som Sak, 2023).

Even with these developments, the availability of digital bookkeeping applications is not a sufficient condition for their proper utilisation. Effectiveness in this context goes beyond feature sets to include how well these tools address the needs of the users, enhance financial accuracy, and enable competitive performance in situations with resource-constrained SMEs (Sarawagi et al., 2024). In this study, perceived effectiveness is the belief of users about a system’s degree to achieve its intended outcomes (such as improved task performance, better decision quality, time savings, or reduced costs), and not just being easy to use or useful. The successful adoption is determined by usability, quality of the system, perceived usefulness, and, more importantly, whether the user is satisfied with the application, which can affect long-term adoption and value realisation (Ilyas et al., 2023). Strong user satisfaction, which can be described as the level at which end users believe that the digital bookkeeping application is addressing or even surpassing their expectations in practice, is critical since it leads to continuance intentions, lower resistance, and greater integration into business processes (Mouhcine, 2021).

Adoption of technology and satisfaction can be comprehended from Technology Acceptance Model (TAM). As per its key elements in shaping the user intention and attitude for technology adoption are perceived usefulness and perceived ease of use (Aburbeian et al., 2022). Researchers have developed TAM to incorporate post-adoption variables like user satisfaction and continuance intention as they have realised that initial acceptance is not necessarily followed by continued and successful use without positive user experiences (Ilyas et al., 2023). Although TAM was initially applied in general information systems research, its relevance to digital accounting and bookkeeping solutions is a fairly well-established and useful tool that can be used to model user-centric outcomes in SMEs.

There are empirical evidences related to these constructs, but research in the UK SME context that study digital bookkeeping effectiveness and user satisfaction are limited. For instance, research by (Al-hattami & Almaqtari, 2023) studied SME’s continuance intention for digital accounting systems using models like Expectation-Confirmation Model, Information System Success Model, and TAM. They found significant association of system quality, information quality, perceived usefulness, ease of use, and satisfaction with intention to use digital accounting systems continues. This implies that satisfaction is not just a passive factor, but it is an active mediating factor of technology use and success. Another empirical research examined the use of digital accounting apps among SMEs through the lens of user-centricity by assessing user ratings and feedback across apps (Sarawagi et al., 2024). Though the study was not utilising a UK sample and PLS-SEM analysis, it pointed to the fact that there are vastly different user experiences as some apps (e.g., “myBillBook” and “Zoho Books”) are relatively well-received by users, whereas others (e.g., “Xero Accounting” in the given sample) are prone to user dissatisfaction due to the lack of features or cost perceptions. These results are an indication of the value of contextualised user feedback to determine effectiveness and satisfaction in terms of feature lists or adoption rates.

However, there are still gaps in the literature. There are no UK-specific studies that combine these constructs with the mediating effect of user satisfaction on the effectiveness of digital bookkeeping tools and the ultimate outcomes (perceived effectiveness, intention to continue, and overall benefit of operations) (Ilyas et al., 2023; Sarawagi et al., 2024). This is a notable gap in the knowledge about how the UK SMEs experience and evaluate digital bookkeeping tools in practice.

The importance of this study is that it investigates the post-adoption assessment of digital bookkeeping technologies in the highly regulated and digitally mature UK SME context. In contrast to previous studies that mostly focused on adoption intention or continuance intention, this study assesses perceived effectiveness as an operational outcome related to the workflow integration, the decision support, financial accuracy, and regulatory compliance. The other importance of the research is that the activity of UK SMEs is increasingly becoming digital reporting under the influence of such initiatives as Making Tax Digital, and user satisfaction and experience turn out to be the keys to sustainable technology usage. Accordingly, the results offer theoretical and practical understanding of how digital bookkeeping solutions are assessed following implementation and how contentment leads to the perceived organisational worth in the context of SMEs. Practically, the results of this research assist software developers, policymakers, and SME practitioners to focus on design-related improvements, training, and support alternatives, which lead to increased user satisfaction, more successful utilisation of the technology, and better financial results.

2. LITERATURE REVIEW

2.1. Theoretical Framework

Technology Acceptance Model (TAM), developed by Fred Davis, is an information systems theory that explains as well as forecast technology adoption and its usage by individuals.

(Mark, 2024) addressed that as per this model perceived ease of use (the degree to which a user is convinced that the technology is effort-free) and the perceived usefulness (the degree to which a user is convinced that technology helps to enhance performance) are the two cognitive beliefs that determines the user’s behavioural intention to use the technology/system. These beliefs affect attitudes and intentions, and these determine actual usage behaviour. TAM is suitable in terms of studing current study’s subject matter. In current study, this concept is the perception of SMEs regarding improvement in decision-making, accuracy, and compliance through bookkeeping software. Secondly, the SME’s perception regarding how easy the system is to use is perceived ease of use. These constructs assist in understanding the attitude of users to adoption and, more importantly, the relationship between these attitudes and satisfaction as well as continuation of use.

TAM has been effectively employed in empirical research studies with a similar technology context. Indicatively, (Song et al., 2025) used TAM to investigate how AI technology is adopted in business management and found that the constructs of perceived usefulness are core determinants of acceptance and outcomes of organisations. Furthermore, a TAM-based study on the uptake of mobile accounting applications in SMEs suggested that the perceptions of usefulness and the ease of use had a significant impact on intentions to use, which confirms the applicability of the framework to the accounting-related systems (Kholid & Asri, 2021). However, this study explicitly applied the user satisfaction as a mediator as the TAM framework’s subset, thereby offering a more comprehensive view of the way SMEs not only accept but also evaluate and keep up the use of digital bookkeeping technologies practically.

Secondly, the researcher first examined various theoretical models that could be employed to justify this study. As an illustration, the Information Systems Success Model (ISSM) of DeLone and McLean, which frames the concept of information system success through the lens of net benefit, service quality, information quality, and system quality, was also taken into account (Çelik & Ayaz, 2022). It was rejected because its high-level systemic nature fails to explicitly oblige user satisfaction as a mediating variable between technology perceptions and perceived effectiveness, which is the focus of this study. Similarly, Unified Theory of Acceptance and Use of Technology (UTAUT), a technology adoption explanation framework that incorporates performance expectancy, effort expectancy, social influence, and facilitating conditions was studied (Momani, 2020). However, it was left out because its orientation on social and organisational issues is not as consistent with the user-based and post-adoption orientation of the UK SMEs which were sampled in the study.

Thus, TAM was finally chosen because it is highly focused on the individual perceptions of users. Even though the original TAM assumes that PEOU is a determinant of PU, the current study is concerned with the post-use analysis of digital bookkeeping tools on UK SMEs.

Prior studies on post-adoption information systems have suggested that the connection established in the initially created TAM may not be as crucial after users have gained significant familiarity with a technology. (Thong et al., 2006) work was based on Expectation-Confirmation Model (ECM) of IT continuance in which authors used perceived usefulness and perceived ease of use as post-adoption’s two isolated constructs, impacting post-adoption satisfaction and continuance among people currently using it. This view points to experienced users evaluating usefulness and ease of use separately based on their established usage experiences. Moreover, (Mishra et al., 2023) re-investigated the post-acceptance information systems continuance models using a meta-analytic structural equation modeling study and noted that post-adoption analyses are increasingly emphasising satisfaction and continuation-related outcomes based on users accumulated experiences with technology. Within well-developed usage contexts, usefulness and ease of use are often considered as simultaneous foundations of post-adoption outcomes, which reflects a move from initial acceptance processes, to experiential analyses of performance of the system.

In post-adoption contexts, users generally have sufficient experience with a system to assess its usefulness and ease of use as distinct cognitive evaluations rather than sequential beliefs. Perceived usefulness and Perceived ease of use are considered in the literature as essential elements for satisfaction and better outcomes after adopting the technology (Thong et al., 2006; Cheng et al., 2023). Considering this, current research is not an adoption or expansion of the well-known route of PEOU→PU route. Instead, this study examines the direct and mediating results of PEOU and PU on user satisfaction and perceived effectiveness in the context of SME and post-implementation.

2.2. Hypotheses Formation

A growing amount of empirical literature has emphasised the critical contribution of PU to technology effectiveness and outcomes. As an example, (Ghani et al., 2022) investigated the impact of digital banking effectiveness by using TAM with 228 bank clients in Malaysia and discovered that perceived usefulness significantly and positively influences the effectiveness of digital banking services, meaning that those clients who perceived the digital financial platform to be useful reported better service outcomes (e.g., convenience and performance). Although the analysis is on banking, as opposed to business bookkeeping, the results have shown that the perceived usefulness directly translates to effectiveness in the financial technology domains. This study, however, only focused on one service setting and not SMEs or business systems in general.

Correspondingly, a study by (Kurniawan et al., 2025) provided findings on both accounting digitalisation and decision-making in the context of 300 SME operators in West Java, Indonesia. Their results supported that digital accounting adoption and the process efficacy for digitally made decisions are significantly impacted by the perceived usefulness. Because it increases the data timeliness and accuracy. It means that not only usefulness perceptions stimulate adoption, but they also have links to improved organisational outcomes. Though it applies to SMEs, the generalisability to the UK environment is restricted due to the fact that the study was conducted in the context of Indonesian SMEs.

Similarly, literature indicated that perceived usefulness of technology has a significant impact on salient results like productivity and performance, which supports the value of usefulness beliefs in the determination of the actual benefits (Bolodeoku et al., 2022). However, it concentrated on the productivity of employees as opposed to the effectiveness of SME systems. Therefore, the overwhelming evidence supports the fact that, as users feel that digital systems are indeed beneficial, such perceptions are correlated with improved performance or effectiveness outcomes. Building on this, H1 is proposed.

H1: Perceived usefulness of digital bookkeeping applications has a positive and significant effect on their perceived effectiveness among UK SMEs.

(Putri et al., 2025) investigated the use of cloud-based accounting in 100 SMEs with applications such as QuickBooks and Xero and found that firm performance was associated with increase in the cloud accounting performance which was due to the perceived ease of use of the system. This shows that in cases where SMEs have an easy time with the digital bookkeeping tools, the systems are more likely to be implemented in business processes successfully; however, the study was geographically limited to the Denpasar SMEs. Another piece of evidence is research on digital management accounting among 225 SMEs in Bangladesh that showed that ease of use was a powerful predictor of the digital accounting system uptake (Begum & Begum, 2025). Even though the given research was aimed at adoption decisions, its results suggest that fewer challenging systems are implemented with less difficulty, which creates an environment that allows them to be effective. Such factors of usability imply that the ease of the system has a direct influence on the ability of SMEs to incorporate digital financial tools into their processes, which makes the concept of easier systems being perceived as more effective. What is lacking is that most of such studies focus on adoption or intention, instead of actually evaluating the outcomes of effectiveness, or are not focused within the UK context. Building on this evidence, H2 is proposed.

H2: Digital bookkeeping applications’ perceived ease of use positively and significantly associated with their perceived effectiveness in UK SMEs.

A number of recent empirical studies highlight the role of user satisfaction in SME technology adoption. Although not every study concentrates only on the bookkeeping or accounting systems, all of them highlight the role of satisfaction, direct or indirect, as a mediating factor in the use of digital technology and performance. A study that is applicable is (Al-Hattami & Almaqtari, 2023), which examined SMEs’ digital accounting system continuance intention. Their study used ECM, ISSM, and TAM, and their results supported that satisfaction was essential for ease of use, perceived usefulness, and continuation used. Despite the focus on continuance rather than on effectiveness, as such, the inclusion of the construct of satisfaction supports that it will play a mediator role in transforming the perceptions regarding the systems into continued use of digital accounting systems.

A different study by (Imtihan et al., 2025) explored features of Accounting Information System (AIS) and their impact on loyalty, decision-making and user satisfaction on 62 Indonesian micro, small and medium enterprises (MSMEs). The study was based on PLS-SEM and established that system quality and ease of use were significant predictors of user satisfaction, and that user satisfaction mediated the impact of system attributes on higher-order outcomes (decision-making and loyalty). This supported the role of satisfaction as an important mediator between technology perceptions and consequential outcomes. Nonetheless, the research was small in size, and its context was country-specific, which limited the generalisability.

The different study on the ease of use and SME performance found that the effects of information quality and ease of use on organisational performance were mediated by end-user satisfaction (Koerniawan et al., 2024). Even though this research was done on a larger information system scale, and not specifically the bookkeeping process, it still shows that user contentment can mediate system characteristics and performance in SME set-ups. Lastly, (Vărzaru, 2022) examined the acceptance of AI technology in managerial accounting through a modified TAM and analysed the data, including 396 accounting professionals. The research concluded that user satisfaction was strongly and positively related to behavioural intention and actual use of AI-based managerial accounting solutions, which means that satisfied users use these technologies more frequently. The findings support the post-adoption aspect of satisfaction. Nevertheless, the study did not consider user satisfaction as a mediator between perceived usefulness, ease of use, and effectiveness results and was constrained by the cross-sectional design. Consequently, the H3 and H4 hypotheses are suggested to test mediating relationships among the UK SMEs in an empirical study. All hypothesised relationships are provided in Table 1.

Table 1. Hypothesis summary table.

| Hypothesis (H) | Associations | Direction Expected |

| 1 | Perceived Usefulness → Perceived Effectiveness | + |

| 2 | Perceived Ease of Use → Perceived Effectiveness | + |

| 3 | Perceived Usefulness → User Satisfaction → Perceived Effectiveness | + |

| 4 | Perceived Ease of Use → User Satisfaction → Perceived Effectiveness | + |

H3: User satisfaction act as mediator between the association of perceived usefulness and the perceived effectiveness of digital bookkeeping applications among UK SMEs.

H4: User satisfaction act as mediator between the association of perceived ease of use and the perceived effectiveness of digital bookkeeping applications among UK SMEs.

2.3. Conceptual Framework

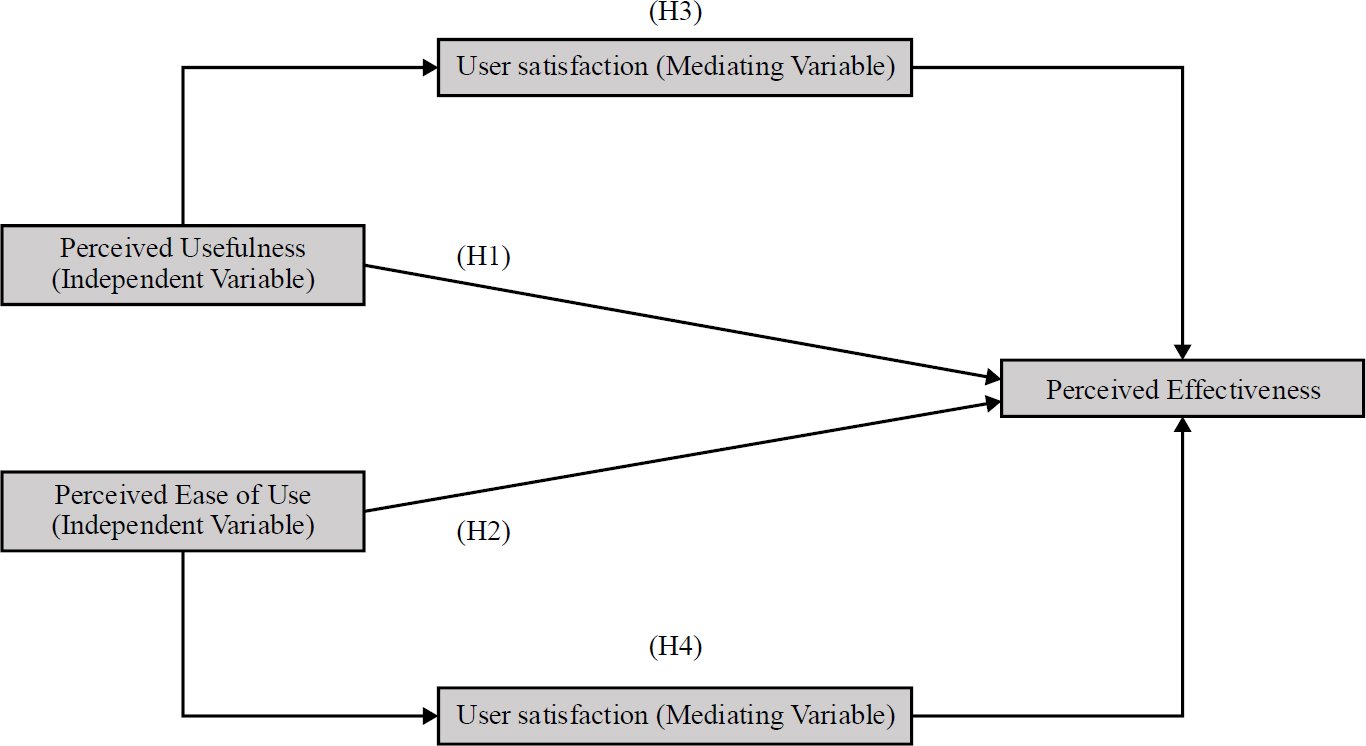

Conceptual framework of this study is depicted in the below Fig. (1). It shows the direct relationship between the dependent variable (perceived effectiveness) and independent variables (perceived usefulness and perceived ease of use). Moreover, user satisfaction is showed as mediating variable, presenting an indirect effect.

Fig. (1). Conceptual framework.

2.4. Literature Gap

Even though there is a growing amount of research on digital accounting and bookkeeping systems, there are still a number of key gaps that are apparent in the present literature. First, many of the previous studies have been predominantly centered on the topic of technology adoption, intention to use, or continuance intention (Kholid & Asri, 2021), as opposed to considering perceived effectiveness as a result, according to the perspective of the user. The studies that do address performance or decision-making outcomes tend to assume that the outcomes are the direct results of using technology without unraveling the psychological mechanisms by which these outcomes are produced (Almgrashi, 2025; Kurniawan et al., 2025). SME literature that focuses on digital accounting, confirms user satisfaction to be essential in post-adoption (Al-Hattami & Almaqtari, 2023; Imtihan et al., 2025; Vărzaru, 2022). But user satisfacation is not studied in bookkeeping setterig for its mediating effect on perceived ease of use and perceived usefulness and effectiveness outcomes. Lastly, the available empirical data is heavily systematised in non-UK contexts (e.g., Indonesia, Jordan, Bangladesh, and South Africa), which restricts contextual transferability in the UK, with a unique regulatory framework and high usage of HMRC-developed digital compliance resources. This study filled these gaps by having a post-adoption and user-centric focus, where directly and indirectly associated constructs (perceived effectiveness, user satisfaction, perceived ease of use, and perceived usefulness) were analyse from UK SMEs sample. The methodology contributes to the theoretical rigor of TAM and gives practically applicable information about the way digital bookkeeping success can be realised in practice, as opposed to being simply adopted.

3. METHODOLOGY

3.1. Research Design

(Thomas & Zubkov, 2023) advocated quantitative design for empirical study especially hypotheses testing which this study employed. The method is suitable for the current study since it attempts to measure the associations between user perceptions of a bookkeeping application and outcome variables like perceived effectiveness and user satisfaction, thus allowing the testing of hypotheses and statistical analysis.

3.2. Data Collection Tool

For data collection a closed-end questionnaire was developed through Google Form with likert scale. The questionnaire included items that measured perceived effectiveness, user satisfaction, perceived ease of use, and perceived usefulness (Appendix A). All of these items were conceptualised as a reflection of the respondents’ evaluative perceptions towards their firm’s use of bookkeeping application.

Perceived usefulness was evaluated using questions that evaluated how much the bookkeeping application enhances financial accuracy, regulatory compliance, decision-making, and the overall financial performance of managing the financial management. Perceived ease of use was used as the measure of the simplicity and the usability of the application interface and functions, and user satisfaction was used as the measure of the user experience and trust in the system. The perceptions of effectiveness were quantified based on operational results which were related to bookkeeping efficiency, financial process control, information organisation, and effectiveness of activities of day-to-day financial management. The distribution of the survey was through Google form, which, as per (Kumar, 2021), is a fast and cost-effective method.

3.3. Population, Sampling Technique, and Sample Size

The population of this study were UK’s small and medium-sized enterprises (SMEs), where employees are not more than 250 employees (European Commission, 2024). SMEs represent more than 99% of the UK business population and play a significant role in the overall employment and economic performance of the country, and therefore, their context is highly pertinent when studying the perception of technology in the actual business setting (Hart et al., 2020). The sampling strategy used was purposive, in which the researcher selected the respondents based on their respective organisational position, like owners, managers, accountants, and finance officers, and their direct exposure to the bookkeeping practices. This strategy is used to make sure that respondents are qualified and have the responsibility to make decisions that are informed and valid (Tajik et al., 2025), and it is specifically suitable when the focus of the research is on particular knowledge holders instead of the general population. Nonetheless, LinkedIn-based purposive sampling procedure can bias digitally mature SMEs and companies that are already active participants in online professional networks.

The data were gathered through LinkedIn invitations, which provided 545 responses, with 500 being complete and usable responses after the screening. This is larger than the recommended minimum sample size, with G*Power indicating at least 100 respondents to identify a medium effect size (0.5) with power of 0.80 and significance of 0.05 probability (Kang, 2021). In such a way, the final sample of 500 is sufficient in terms of statistical power and improves the strength and external validity of the results. Moreover, statistical power analysis, i.e., minimum R2-based techniques, underlies the rationale of using larger samples in PLS-SEM, specifically in models that imply mediation and latent constructs (Hayes, 2021).

3.4. Data Analysis

PLS-SEM or Partial Least Squares Structural Equation Modelling method was used to analyse the data collected. As per (Memon et al., 2021), it is suitable to predict and explain models with the use of latent variables. PLS-SEM is favoured where a model structure is complicated, non-normal data distribution, and mediation effects are involved, and it is, therefore, suitable for the goals of this research (Ahmed et al., 2024).

It was selected because it can test both direct and indirect associations. The constructs were all modelled as reflective because all indicators were supposed to reflect the underlying latent variable and not constitute it. This specification is in line with the conceptualisation that the responses to the survey are an expression of respondents’ perceptions of the bookkeeping application in terms of being useful, easy to use, satisfying, and efficient, which can reliably be estimated and interpreted in the PLS-SEM framework.

3.5. Common Method Bias

Common method bias (CMB) was checked to reduce research bias and for that Harman’s single-factor test was conducted. The test uses exploratory factor analysis to confirm if the measurement items’ variance explained by a single factor is less than 50%, showing not significant bias (Howard et al., 2024). In the given research, the initial factor contributed to the total variance by 38.7%, which proved that the issue of CMB did not pose a serious problem. The assessment of non-response bias was conducted through the comparing of early and late respondents using independent sample tests, adhering to the accepted practices, including those suggested by (Armstrong & Overton, cited in France et al., 2023). According to survey research literature, the average response rate of online surveys is 15-20%, and it is important to measure non-response bias when there is a possibility that respondents are not representative of non-respondents (Bhattacherjee, 2019). Early and late responses of 30 respondents were analysed and the constructs showed no significant differences from the rest of the respondents. This supports that the results were not impacted by the non-response bias significantly. Moreover, another approach to ensure that CMB is not a significant issue is to confirm that the full collinearity VIF values of all constructs are above 3.3. Table 2 shows that all the values fulfil this criterion, thus CMB is not a serious issue here.

Table 2. Collinearity statistics (VIF).

| – | VIF |

| Perceived Ease of Use | 1.412 |

| Perceived Usefulness | 1.811 |

| User Satisfaction | 1.713 |

3.6. Ethical Consideration

Lastly, the study was conducted with ethical consideration. These involved informed consent, voluntary participation, anonymity and confidentiality, and secure data handling procedures to protect the study participants and the integrity of the research. Participants were informed about the purpose of the study, its procedures, and their rights in a clear way beforehand. Transparency and autonomy are key best practices in online survey research (Kang & Hwang, 2023; Stokes, 2025). No personal identifiable data was gathered, and all answers were stored safely to protect privacy, as required by the existing ethical standards in conducting internet-based research. All these actions served to adhere to the ethical guidelines of research involving human subjects.

4. RESULTS

Table 3 presents the demographic characteristic of the 500 respondents, which reveals a balanced age distribution with the highest percentage of 35-44 (31.2%) and 25-34 (28.4%), indicating that the users are of the mid-career SMEs segment. The proportion of males (55.2%) is a bit more than that of females (39.6%), and a minor percentage are non-binary or do not state it. The majority of the respondents are owners (37.6%) and managers (20.4%). The leading sectors are Services (33.6%) and Retail (24.8%). Most have been using digital bookkeeping solutions for 1-3 years (37.2%), followed by 4-6 years (30.8%) and more than 6 years (17.2%), which shows consistent use of digital solutions.

Table 3. Demographic analysis.

| Category | Group | Frequency (n) | Percentage (%) |

| Age | Under 25 | 58 | 11.6 |

| 25–34 | 142 | 28.4 | |

| 35–44 | 156 | 31.2 | |

| 45–54 | 96 | 19.2 | |

| 55 and above | 48 | 9.6 | |

| Gender | Male | 276 | 55.2 |

| Female | 198 | 39.6 | |

| Non-binary | 12 | 2.4 | |

| Prefer not to say | 14 | 2.8 | |

| Position in the Business | Owner | 188 | 37.6 |

| Partner | 64 | 12.8 | |

| Manager | 102 | 20.4 | |

| Accountant | 86 | 17.2 | |

| Finance Officer | 44 | 8.8 | |

| Other | 16 | 3.2 | |

| Industry Sector | Retail | 124 | 24.8 |

| Manufacturing | 82 | 16.4 | |

| Services | 168 | 33.6 | |

| Construction | 58 | 11.6 | |

| Technology | 52 | 10.4 | |

| Other | 16 | 3.2 | |

| Years Using Digital Bookkeeping Applications | Less than 1 year | 74 | 14.8 |

| 1–3 years | 186 | 37.2 | |

| 4–6 years | 154 | 30.8 | |

| More than 6 years | 86 | 17.2 |

The results of the measurement model are introduced in Table 4, and they are calculated with the help of measurement model. The measurement model is used to assess the reliability of indicators, internal consistency, as well as convergent validity, which are essential components of construct measurement in SEM (Hair et al., 2021). All constructs in this research satisfy these thresholds, and thus it is clear that the items are good measures of perceived effectiveness, ease of use, usefulness, and user satisfaction, which attests to the quality of the measurement.

Table 4. Measurement model assessment.

| Latent Construct | Indicator | Factors Loading | Cronbach’s Alpha | Composite Reliability | Average Variance Extracted (AVE) |

| Perceived Effectiveness | PE1 | 0.908 | 0.904 | 0.940 | 0.838 |

| PE2 | 0.932 | ||||

| PE3 | 0.906 | ||||

| Perceived Ease of Use | PEOU1 | 0.815 | 0.825 | 0.895 | 0.741 |

| PEOU2 | 0.899 | ||||

| PEOU3 | 0.866 | ||||

| Perceived Usefulness | PU1 | 0.876 | 0.845 | 0.906 | 0.763 |

| PU2 | 0.898 | ||||

| PU3 | 0.845 | ||||

| User Satisfaction | US1 | 0.897 | 0.888 | 0.931 | 0.817 |

| US2 | 0.931 | ||||

| US3 | 0.884 |

Note: All constructs meet thresholds; Factor Loadings ≥ 0.70; CR ≥ 0.70; AVE ≥ 0.50 (Hair et al., 2021).

4.1. Discriminant Validity

Table 5 shows the results of discriminant validity based on the HTMT criterion, which as per (Henseler, 2026), examines whether constructs are empirically different in the model of measurement. Discriminant validity is defined as the degree to which theoretically distinct constructs are practically dissimilar (Afthanorhan et al., 2021). The value of HTMT that is below a conservative level of 0.85 would suggest sufficient discriminant validity among constructs (Cheung et al., 2023). Table 5 presents that all of the HTMT values are not more than 0.85, which support that user satisfactiom, perceived usefulness, and perceived ease of use are not similar constructs and, thus, the interpretation of relationships in the model can be considered structural.

Table 5. Discriminant validity.

| – | Perceived Ease of Use | Perceived Effectiveness | Perceived Usefulness |

| Perceived Effectiveness | 0.469 | – | – |

| Perceived Usefulness | 0.602 | 0.610 | – |

| User Satisfaction | 0.535 | 0.734 | 0.714 |

Note: HTMT values < 0.85

4.2. Path Coefficient

Table 6 displays the results of the structural model and gives the path coefficients, t-statistics, p-values as well as effect sizes (f2) to test the hypotheses proposed. The results indicate differences in the extent of the explanatory power of the constructs; were user satisfaction and perceived usefulness exhibit stronger effects than perceived ease of use.

Table 6. Path coefficient.

| – | Path Coefficient | T-statistics | P-values | f-square |

| Direct Effect | ||||

| Perceived Ease of Use -> Perceived Effectiveness | 0.080 | 1.350 | 0.177 | 0.008 |

| Perceived Ease of Use -> User Satisfaction | 0.198*** | 3.539 | 0.001 | 0.052 |

| Perceived Usefulness -> Perceived Effectiveness | 0.176*** | 2.726 | 0.006 | 0.032 |

| Perceived Usefulness -> User Satisfaction | 0.522*** | 10.235 | 0.001 | 0.347 |

| User Satisfaction -> Perceived Effectiveness | 0.512*** | 8.690 | 0.001 | 0.285 |

| Total and Specific Indirect Effect | ||||

| User Satisfaction -> Perceived Effectiveness | 0.512*** | 8.690 | 0.001 | – |

| Perceived Ease of Use -> User Satisfaction -> Perceived Effectiveness | 0.101*** | 3.290 | 0.001 | – |

Note: Significant paths are indicated using asterisks: *** = p < 0.01 (1%).

The findings show that the perceived usefulness significantly and positively correlates with the perceived effectiveness (β = 0.176, t = 2.726, p = 0.006, f2 = 0.032). This indicates that SMEs who consider digital bookkeeping applications useful are more apt to consider them helpful in facilitating the bookkeeping and financial management processes. The relationship is statistically significant though the effect size is small. Thus, H1 is accepted.

The results demonstrate that, there is no significant direct association between perceived ease of use and perceived effectiveness (β = 0.080, t = 1.350, p = 0.177, f2 = 0.008). This implies that the ease of use is not a conclusive factor in determining the effectiveness of digital bookkeeping applications in the UK SMEs. There is also a negligible effect size which means that the explanatory contribution is weak. Thus, H2 is rejected.

User satisfaction showed significant mediation effect on the association between the perceived usefulness and the perceived effectiveness (β = 0.267, p = 0.001). In addition, perceived usefulness significantly influences user satisfaction (β = 0.522, t = 10.235, p = 0.001, f² = 0.347), while user satisfaction significantly predicts perceived effectiveness (β = 0.512, t = 8.690, p = 0.001, f² = 0.285). The relationships are both significant, and thus, the mediation is partial. Because the perceived usefulness and effectiveness are directly and indirectly associated through a mediator. Thus, H3 is accepted.

The findings also suggest that user satisfaction is a strong mediator between perceived ease of use and perceived effectiveness (β = 0.101, p = 0.001, t = 3.290). The relationship between perceived ease of use and perceived effectiveness is not significant (β = 0.198, t = 3.539, p = 0.001, f2 = 0.052) but the relationship between perceived ease of use and user satisfaction is significant (β = 0.198, t = 3.539, p = 0.001, f2 = 0.052). Since the direct association between perceived ease of use and perceived effectiveness was not significant, this mediation through user satisfaction is complete. H4 is thus accepted.

Combined, the findings suggests that in the UK SMEs, conversion of user perception for digital bookkeeping applications into perceptions of effectiveness is mediated by user satisfaction.

4.3. Model Explanatory Power and Predictive Relevance

Table 7 presents the explanatory power of the model through the values of R-squared, which (Hair et al., 2021) defined as the degree to which the exogenous constructs account for endogenous constructs variance. The greater the R-squares, the better the explanatory power. In this research, the model moderately explains perceived effectiveness (0.463) and user satisfaction (0.416) whereby perceived usefulness and ease of use, mediated by a satisfaction, significantly explains the differences in effectiveness and satisfaction. Moreover, the Q-square value greater than zero shows that for endogenous constructs predictive capability exists in the model. The Q-square values in Table 7 show satisfactory predictive relevance.

Table 7. Model R-square and Q-square values.

| – | R-square | R-square adjusted | Q-Square |

| Perceived Effectiveness | 0.463 | 0.459 | 0.298 |

| User Satisfaction | 0.416 | 0.413 | 0.404 |

5. DISCUSSION

H1: Perceived Usefulness and Perceived Effectiveness.

H1 is supported as the study found a positive and significant association between perceived usefulness and perceived effectiveness (β = 0.176, p = 0.006). The effect size, however, is low (f2 = 0.032), which means that, as much as usefulness is an important factor in the perceptions of effectiveness, its contribution as an independent factor is low. This implies that SMEs might not be assessing the effectiveness of bookkeeping in terms of functional usefulness alone, but also using other experiential and contextual criteria. In the context of UK SMEs, digital bookkeeping applications are more probable to be viewed as effective in the case when they enhance the accuracy of financial data, adherence to regulations, and decision-making. The results are in line with (Ghani et al., 2022; and Kurniawan et al., 2025) who linked usefulness perceptions with better organisational performance in digital accounting settings.

Usefulness in this study is not studied as the motivation of the adoption for the technology but the evaluation of its performance post-adoption. SMEs operating within the scope of HMRC-related compliance demands might be more concerned with the reliability of the functioning and practical value following the incessant use of a system than with the technological novelty. This result answers the research question of whether digital bookkeeping systems are operationally effective once implemented, as opposed to adopted. One practical implication is that software vendors can gain by focusing on the output-based characteristics like accuracy of reporting, compliance support, and financial decision support to enhance long-term effectiveness perceptions among SMEs.

H2: Perceived Ease of Use and Perceived Effectiveness

H2 is rejected as the result showed non-significant association between perceived ease of use and perceived effectiveness (β = 0.080, p = 0.177). The effect size is also insignificant (f2 = 0.008), meaning that ease of use has a minimal contribution to the explanation of the effect on the perception of the effectiveness independently. This means that usability might not necessarily have a direct effect on the effectiveness of digital bookkeeping applications as assessed by UK SMEs in post-adoption environments. One fact that might explain it is that a lot of SMEs that already work in digitally advanced surroundings already demand bookkeeping systems to meet the minimum standards of usability. Ease of use can thus cease to be a significant point of distinction when the technology is already implemented and used regularly.

The results are contrasted with others like (Begum & Begum, 2025; and Putri et al., 2025) which established direct usability-performance links in less developed adoption settings. The present results indicate that the perceptions of effectiveness in UK SMEs are more tightly linked to operational reliability, workflow integration, and practical outcomes than interface simplicity. It is important to note that this finding is not evaluation of initial acceptance behaviour but an evaluation of post-adoption technology. One of the practical implications is that organisations adopting bookkeeping software might have to integrate usability-enhancing features with workflow support, training, and integration to enhance the perceptions of operational effectiveness.

H3: Mediating Role of User Satisfaction between Perceived Usefulness and Perceived Effectiveness

H3 is supported as current results supported the mediator role of use satisfaction for perceived usefulness and perceived effectiveness relationship (β = 0.267, p = 0.001). Since the indirect and direct association are significant, the mediation is partial. Moreover, the perceived usefulness shows a significant impact on the user satisfaction (f2 = 0.347), which proves usefulness as a critical predictor of the positive user experiences in the digital bookkeeping settings. This implies that SMEs consider bookkeeping applications as effective not just due to the functional value, but also due to the fact that useful systems promote confidence, trust and satisfaction in terms of continued use.

These results are in line with (Al-Hattami & Almaqtari, 2023; and Imtihan et al., 2025) who discovered that satisfaction reinforces the connection between system characteristics and post-adoption results. The partial mediation also indicates that usefulness has both direct evaluative and indirect experiential role via satisfaction. In the UK SMEs, beneficial bookkeeping functions can solidify on perceptions of reliability and regulatory support, which in turn intensifies effectiveness judgments. Considering that this study only investigated only UK SMEs through purposive sampling and LinkedIn recruitment, it is important to cautiously take the mediation effect. The practical implication is that companies that adopt bookkeeping systems must not only consider some of the functional utility of the software, but they must consider the satisfaction of users in the process of having long-term interaction with the system.

H4: User Satisfaction as a Mediator of the Relationship between Perceived Ease of Use and Perceived Effectiveness

The results confirm the H4 hypothesis since the user satisfaction lies between the perceived ease of use and perceived effectiveness (β = 0.101, p = 0.001). The perceived ease of use has a small effect size on user satisfaction (f2 = 0.052) and so usability is a contributing factor to user satisfaction, but to a smaller degree than perceived usefulness. The mediation is complete since the direct correlation between perceived ease of use and perceived effectiveness is not significant. It means that ease of use can only add to the perceptions of effectiveness when it enhances the user experience and satisfaction in general.

These results are consistent with those of (Koerniawan et al., 2024), who found that satisfaction was a mediator between system features and SME performance outcomes and with (Vărzaru, 2022), who asserted that satisfaction is a significant post-adoption variable in the use of accounting technologies. Reducing frustration, effort in learning and reliance on external support may help to improve positive experiences in the UK SMEs, which in turn enhances perceptions of effectiveness. To a certain degree, these findings can be used to help solve the research problem by demonstrating that usability does not necessarily result in positive operational ratings unless it is supported by satisfactory user experiences. A practical suggestion is that organisations can leverage onboarding assistance, user documentation, and continuous support instead of just depending on the simplicity of the interface to enhance long-term system reviews.

THEORETICAL CONTRIBUTION

The contribution of current findings is that it provides TAM contextual extension within a set-up which is controlled and for SMEs that are digitally advanced.As opposed to the conventional TAM studies, which primarily address the intention of adoption, the current study considers perceived effectiveness as the post-adoption operational outcome, which is linked to the workflow integration, decision support, financial management and regulatory compliance. Usefulness as per current findings is not just a adoption related belief but more a confirmation of performance created from continues interaction with system.

The paper also explains the clear differentiation between the perceived usefulness, the perceived ease of use, and user satisfaction regarding the post-adoption assessment. Findings reveal that the perceived usefulness has both direct and satisfaction-mediated relationships with effectiveness, but perceived ease of use has no direct relationship with effectiveness, but rather an indirect relationship with effectiveness through satisfaction. Moreover, the comparatively low direct effects indicate that the perceptions about the effectiveness of bookkeeping are influenced by various organisational and experiential characteristics not limited to core constructs of TAM. This brings out the contingent and situational characteristics of technology valuation among the UK SMEs. Nevertheless, this can be only understood in the context of the limitations of the UK-specific setting, purposive sampling through LinkedIn and self-reported scales of the study.

CONCLUSION

This paper shows that the perceived effectiveness of digital bookkeeping applications in the UK SMEs is more likely to be influenced by the post adoption evaluation process than the initial acceptance. The practicality of systems in promoting credible financial control, regulation, and daily choice procedures is what promotes effectualness. These findings indicate that effectiveness judgments in SMEs are made by a mixture of system performance and user experience, specifically, by satisfaction-based evaluation. Digital bookkeeping effectiveness is generally a gained experience with the ongoing use of the system in actual operating environments.

LIMITATIONS AND FUTURE DIRECTION

To begin with, the research utilised cross-sectional self-reported data, which restricted causal inference and created a risk of common methods bias despite the high standards of statistical tests. Future studies need to embrace longitudinal designs to help in capturing the variations in user satisfaction and efficacy perception over long intervals of technology use. Moreover, moderating variables, including digital literacy, firm size, regulatory knowledge, and accounting expertise, are the recommended areas that should be studied by researchers in order to gain a clearer understanding of conditional effects. Further research needs to be directed at one bookkeeping software (e.g., Xero or QuickBooks) in a particular sector, e.g., retail or service. Further, the addition of objective performance measures (VAT filing accuracy, timeliness of reporting, the rates of errors reduction, and cost savings) would enhance empirical soundness.

POLICY IMPLICATIONS

To policymakers, the results highlight the importance of designing digital compliance programmes, like Making Tax Digital, to actively include SME user feedback and usability testing to make it feasible. Software developers are encouraged to emphasise on making navigation easier, incorporating guided tutorials, and other context-specific support tools that increase user satisfaction more than merely adding complicated features. To improve the effectiveness of bookkeeping, SME owners and managers should carry out organised training, select the application that fits their level of transaction and reporting needs, and monitor user experience indicators on a regular basis. Financial advisories and professional organisations must consider providing special workshops and advisory services to raise awareness of satisfaction-based implementation strategies that would enable SMEs to adopt digital bookkeeping practices with a high level of consistency, without errors, and in a timely manner.

LIST OF ABBREVIATIONS

AIS | = | Accounting Information System |

CMB | = | Common Method Bias |

ECM | = | Expectation-Confirmation Model |

ISSM | = | Information Systems Success Model |

SMEs | = | Small and Medium-Sized Enterprises |

MSMEs | = | Micro Small and Medium Enterprises |

PLS-SEM | = | Partial Least Squares Structural Equation Modelling |

TAM | = | Technology Acceptance Model |

UTAUT | = | Unified Theory of Acceptance and Use of Technology |

AUTHOR’S CONTRIBUTION

A.B has contributed to the study conceptualization, methodology, data analysis, interpretation of results, and manuscript writing.

ETHICAL APPROVAL & INFORMED CONSENT

The study was conducted with ethical consideration. These involved informed consent, voluntary participation, anonymity and confidentiality, and secure data handling procedures to protect the study participants and the integrity of the research. Participants were informed about the purpose of the study, its procedures, and their rights in a clear way beforehand. Transparency and autonomy are key best practices in online survey research (Kang & Hwang, 2023; Stokes, 2025). No personal identifiable data was gathered, and all answers were stored safely to protect privacy, as required by the existing ethical standards in conducting internet-based research. All these actions served to adhere to the ethical guidelines of research involving human subjects.

AVAILABILITY OF DATA AND MATERIALS

The data will be made available on reasonable request by contacting the corresponding author [A.B].

FUNDING

None.

CONFLICT OF INTEREST

The author declare that there is no conflict of interest regarding the publication of this article.

ACKNOWLEDGEMENTS

Declared none.

DECLARATION OF AI

During the preparation of this manuscript, the author used ChatGPT for language editing and refinement purposes. Following the use of this tool, the author carefully reviewed and revised the content where necessary and accept full responsibility for the final published version of the article.

APPENDIX A

Questionnaire

Section A: Demographic Information

- Age

- ☐ Under 25

- ☐ 25–34

- ☐ 35–44

- ☐ 45–54

- ☐ 55 and above

- Gender

- ☐ Male

- ☐ Female

- ☐ Non-binary

- ☐ Prefer not to say

- Current Position in the Business

- ☐ Owner

- ☐ Partner

- ☐ Manager

- ☐ Accountant

- ☐ Finance Officer

- ☐ Other

- Industry Sector

- ☐ Retail

- ☐ Manufacturing

- ☐ Services

- ☐ Construction

- ☐ Technology

- ☐ Other

- Years Using Digital Bookkeeping Applications

- ☐ Less than 1 year

- ☐ 1–3 year/s

- ☐ 4–6 years

- ☐ More than 6 years

Measurement Items and Likert Scale

Scale:

- 1 = Strongly Disagree

- 2 = Disagree

- 3 = Neutral

- 4 = Agree

- 5 = Strongly Agree

| Construct | Code | Measurement Item | 1 | 2 | 3 | 4 | 5 |

| Perceived Usefulness (PU) | PU1 | The bookkeeping application at my firm improves the accuracy of financial records. | ☐ | ☐ | ☐ | ☐ | ☐ |

| PU2 | The bookkeeping application helps our firm comply with tax and regulatory requirements. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| PU3 | The bookkeeping application supports better financial decision-making for the firm. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| PU4 | The bookkeeping application reduces errors in bookkeeping tasks. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| PU5 | The bookkeeping application adds measurable value to our firm’s financial management. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| Perceived Ease of Use (PEU) | PEU1 | Learning to use the bookkeeping application at my firm was easy. | ☐ | ☐ | ☐ | ☐ | ☐ |

| PEU2 | The interface of the bookkeeping application is clear and intuitive. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| PEU3 | I can complete bookkeeping tasks quickly using the bookkeeping application. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| PEU4 | Navigating through the bookkeeping application is straightforward. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| PEU5 | I can use the bookkeeping application efficiently without much assistance. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| User Satisfaction (US) | US1 | I am satisfied with how the bookkeeping application performs in my firm. | ☐ | ☐ | ☐ | ☐ | ☐ |

| US2 | The bookkeeping application meets my expectations for managing financial tasks. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| US3 | Using the bookkeeping application is a positive experience. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| US4 | I feel confident relying on the bookkeeping application for accurate records. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| US5 | Overall, I am pleased with the results achieved using the bookkeeping application. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| Perceived Effectiveness (PE) | PE1 | The bookkeeping application effectively supports day-to-day bookkeeping activities at my firm. | ☐ | ☐ | ☐ | ☐ | ☐ |

| PE2 | The bookkeeping application helps maintain accurate and timely financial records. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| PE3 | The bookkeeping application enhances control over financial processes. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| PE4 | Using the bookkeeping application improves the organisation of financial information. | ☐ | ☐ | ☐ | ☐ | ☐ | |

| PE5 | The bookkeeping application contributes to overall efficiency in managing our firm’s finances. | ☐ | ☐ | ☐ | ☐ | ☐ |

REFERENCES

Aburbeian, A. M., Owda, A. Y., & Owda, M. (2022). A technology acceptance model survey of the metaverse prospects. AI, 3(2), 285-302.

https://doi.org/10.3390/ai3020018

Adler, T. (2021). Best UK small business accounting software – review guide. Small Business UK. Available from: https://smallbusiness.co.uk/best-uk-small-business-accounting-software-review-guide-2548848/ (Accessed on: 22 May, 2026).

Afthanorhan, A., Ghazali, P.L. & Rashid, N. (2021). Discriminant validity: A comparison of CBSEM and consistent PLS using Fornell & Larcker and HTMT approaches. Journal of Physics: Conference Series, 1874(1), 012085.

https://doi.org/10.1088/1742-6596/1874/1/012085

Ahmed, R. R., Streimikiene, D., Streimikis, J., & Siksnelyte-Butkiene, I. (2024). A comparative analysis of multivariate approaches for data analysis in management sciences. E+ M Ekonomie a Management., 27(1), 192-210.

https://doi.org/10.15240/tul/001/2024-5-001

Al-Hattami, H. M., & Almaqtari, F. A. (2023). What determines digital accounting systems’ continuance intention? An empirical investigation in SMEs. Humanities and Social Sciences Communications, 10(1), 1-13.

https://doi.org/10.1057/s41599-023-02332-3

Almgrashi, A. (2025). The influence of the digital accounting system on the quality of sustainable decision-making. Journal of Risk and Financial Management, 18(11), 602.

https://doi.org/10.3390/jrfm18110602

Begum, R., & Begum, F. (2025). Digitalization of management accounting in small and medium enterprises: Expansion of the technology acceptance model. Corporate Governance and Sustainability Review, 9(2), 91-99.

https://doi.org/10.22495/cgsrv9i2p8

Bhattacherjee, A. (2019). Survey research. In Social science research: Principles, methods, and practices (Rev. ed., Chapter 9). Pressbooks. Available from: https://usq.pressbooks.pub/socialscienceresearch/chapter/chapter-9-survey-research/

Bolodeoku, P.B., Igbinoba, E., Salau, P.O., Chukwudi, C.K. and Idia, S.E. (2022). Perceived usefulness of technology and multiple salient outcomes: the improbable case of oil and gas workers. Heliyon, 8(4), e09322.

https://doi.org/10.1016/j.heliyon.2022.e09322

Çelik, K., & Ayaz, A. (2022). Validation of the Delone and McLean information systems success model: a study on student information system. Education and Information Technologies, 27(4), 4709-4727.

https://doi.org/10.1007/s10639-021-10798-4

Cheung, G.W., Cooper-Thomas, H.D., Lau, R.S. & Wang, L.C. (2024). Reporting reliability, convergent and discriminant validity with structural equation modeling: A review and best-practice recommendations. Asia Pacific Journal of Management, 41, 745-783.

https://doi.org/10.1007/s10490-023-09871-y

European Commission (2024). SME definition – European Commission. single-market-economy.ec.europa.eu. Available from: https://single-market-economy.ec.europa.eu/smes/sme-fundamentals/sme-definition_en

France, S. L., Adams, F. G., & Landers, V. M. (2023). Worst case resistance testing: A nonresponse bias solution for today’s behavioral research realities. arXiv preprint arXiv:2301.08377.

https://doi.org/10.48550/arXiv.2301.08377

Ghani, E. K., Ali, M. M., Musa, M. N. R., & Omonov, A. A. (2022). The effect of perceived usefulness, reliability, and COVID-19 pandemic on digital banking effectiveness: Analysis using technology acceptance model. Sustainability, 14(18), 11248.

https://doi.org/10.3390/su141811248

Hair Jr, J. F., Hult, G. T. M., Ringle, C. M., Sarstedt, M., Danks, N. P., & Ray, S. (2021). Evaluation of reflective measurement models. In Partial least squares structural equation modeling (PLS-SEM) using Classroom Companion: Business (pp. 75-90). Cham: Springer International Publishing.

https://doi.org/10.1007/978-3-030-80519-7_4

Hart, M., Prashar, N. & Ri, A. (2020). From the cabinet of curiosities: The misdirection of research and policy debates on small firm growth. International Small Business Journal: Researching Entrepreneurship, 39(1), 3-17.

https://doi.org/10.1177/0266242620951718

Hayes, T. (2021). R-squared change in structural equation models with latent variables and missing data. Behavior Research Methods, 53(5), 2127-2157.

https://doi.org/10.3758/s13428-020-01532-y

Henseler, J. (2026). Henseler’s HTMT Calculator. www.henseler.com. Available from: https://www.henseler.com/htmt.html (Accessed on: 22 Aug, 2014).

Howard, M. C., Boudreaux, M., & Oglesby, M. (2024). Can Harman’s single-factor test reliably distinguish between research designs? Not in published management studies. European Journal of Work and Organizational Psychology, 33(6), 790-804.

https://doi.org/10.1080/1359432X.2024.2393462

Hussain, S. (2025). Comparative study of manual vs digital accounting in SMEs: Efficiency, accuracy, and adoption. Entrepreneurial Economics, 1, 1-6.

https://doi.org/10.13140/RG.2.2.23760.42246

Ilyas, M., ud din, A., Haleem, M. & Ahmad, I. (2023). Digital entrepreneurial acceptance: An examination of technology acceptance model and do-it-yourself behavior. Journal of Innovation and Entrepreneurship, 12(1), 15.

https://doi.org/10.1186/s13731-023-00268-1

Imtihan, K., Mardi, M., Tantoni, A., Bagye, W., & Zulkarnaen, M. F. (2025). Enhancing user satisfaction and loyalty in MSMEs: The role of accounting information systems. Journal of Information Systems and Informatics, 7(1), 714-729.

https://doi.org/10.51519/journalisi.v7i1.1044

Kang, E., & Hwang, H. J. (2023). The importance of anonymity and confidentiality for conducting survey research. Journal of Research and Publication Ethics, 4(1), 1-7.

https://doi.org/10.15722/jrpe.4.1.202303.1

Kang, H. (2021). Sample size determination and power analysis using the G* Power software. Journal of Educational Evaluation for Health Professions, 18.

https://doi.org/10.3352/jeehp.2021.18.17

Kholid, M. N., & Asri, N. (2021). The effect of external variables on mobile accounting app adoption by student entrepreneurs. Journal of Small Business Strategy, 31(5), 38–49.

https://doi.org/10.53703/001c.29816

Kock, N. (2015). Common method bias in PLS-SEM: A full collinearity assessment approach. International Journal of e-Collaboration (IJEC), 11(4), 1-10.

https://doi.org/10.4018/ijec.2015100101

Koerniawan, I., Triatmanto, B., & Zuhroh, D. (2024). The influence of ease of use of information technology, information quality and top management support on SME performance through end user satisfaction: A France study on Semarang city SMEs. International Journal of Accounting, Management, And Economics Research, 2(1), 183-206.

https://doi.org/10.56696/ijamer.v2i1.37

Kumar, M. (2021). Top-notch benefits of Google Forms survey data collection. Medium. Available from: https://marketing-insightsdna.medium.com/top-notch-benefits-of-google-forms-survey-data-collection-f27c7f08c6a6 (Accessed on: 8 Sep, 2021).

Kurniawan, A., Machmud, A., Supardi, E. & Purnamasari, I. (2025). Determinants of Accounting Digitalization and Its Impact on Decision-Making Effectiveness in Small and Medium Enterprises in West Java Indonesia. International Journal of Social Science and Human Research, 8(9), 103.

https://doi.org/10.47191/ijsshr/v8-i9-103

Mark, D. (2024). Technology acceptance model (TAM). EBSCO Information Services, Inc. | www.ebsco.com. Available from: https://www.ebsco.com/research-starters/technology/technology-acceptance-model-tam (Accessed on: 8 Nov, 2024).

Memon, M. A., Ramayah, T., Cheah, J. H., Ting, H., Chuah, F., & Cham, T. H. (2021). PLS-SEM statistical programs: A review. Journal of Applied Structural Equation Modeling, 5(1), 1-14.

https://doi.org/10.47263/JASEM.5(1)06

Mishra, A., Shukla, A., Rana, N. P., Currie, W. L., & Dwivedi, Y. K. (2023). Re-examining post-acceptance model of information systems continuance: A revised theoretical model using MASEM approach. International Journal of Information Management, 68, 102571.

https://doi.org/10.1016/j.ijinfomgt.2022.102571

Mohamad Y., F., & Som Sak, C. (2023). Digital bookkeeping solutions for Micro-, Small & Medium Enterprises (MSMEs) / Fauziah Mohamad Yunus and Dr. Chaleeda Som Sak. In: FBM INSIGHTS. Universiti Teknologi MARA, Kedah, Universiti Teknologi MARA, Kedah, pp. 23-26. Available from: https://ir.uitm.edu.my/id/eprint/100250/1/100250.pdf

Momani, A. M. (2020). The unified theory of acceptance and use of technology: A new approach in technology acceptance. International Journal of Sociotechnology and Knowledge Development (IJSKD), 12(3), 79-98.

https://doi.org/10.4018/IJSKD.2020070105

Mouhcine, H. B. (2021). The Role of User Satisfaction in Continuance Intention to Use Chatbots within the Technology Acceptance Model (TAM) (Master’s Thesis, Marmara Universitesi (Turkey). Available from: https://openaccess.marmara.edu.tr/entities/publication/c04507d5-2980-4dba-8d3b-6bdbf9d4283f (Accessed on: 13 Jan, 2026).

Putri, N. P. A. N., Permana, G. P. L., & Mohaidin, N. J. (2025). Perception and Digital Transformation: A Study of Cloud Accounting Adoption among SMEs in Denpasar. Reviu Akuntansi, Manajemen, Dan Bisnis, 5(2), 413–428.

https://doi.org/10.35912/rambis.v5i2.5505

Sarawagi, A., Gupta, A., Singh, M. S., & Bhadouria, S. S. (2024). Evaluating the effectiveness of digital accounting applications for small and medium enterprises: A user-centric approach. Asian Journal of Management and Commerce, 5(2), 01-07.

https://doi.org/10.22271/27084515.2024.v5.i2a.323

Song, Y., Qiu, X., & Liu, J. (2025). The impact of artificial intelligence adoption on organizational decision-making: An empirical study based on the technology acceptance model in business management. Systems, 13(8), 683.

https://doi.org/10.3390/systems13080683

Stokes, M.X. (2025). Best Practices for Anonymous Survey Research Frequently Asked Questions What makes a survey ‘anonymous’? Available from: https://irb.smumn.edu/wp-content/uploads/sites/26/2025/09/Best-practices-for-anonymous-survey-research.pdf (Accessed on: 09 July, 2025).

Tajik, O., Golzar, J., & Noor, S. (2025). Purposive sampling. International Journal of Education & Language Studies, 2(2), 1-9.

https://doi.org/10.22034/ijels.2025.490681.1029

Thomas, D., & Zubkov, P. (2023). Quantitative research designs. In Quantitative Research for Practical Theology, pp. 103-114. Available from: https://www.researchgate.net/publication/370630979_Quantitative_Research_Designs

Thong, J. Y., Hong, S. J., & Tam, K. Y. (2006). The effects of post-adoption beliefs on the expectation-confirmation model for information technology continuance. International Journal of human-computer studies, 64(9), 799-810.

https://doi.org/10.1016/j.ijhcs.2006.05.001

UNCDF (2021). A digital bookkeeping App to Improve Access to Finance A case study from Ghana. Available from: https://www.rfilc.org/wp-content/uploads/2021/11/A-digital-bookkeeping-app-to-improve-access-to-finance-Ghana-1.pdf (Accessed on: Nov, 2011).

Vărzaru, A. A. (2022). Assessing artificial intelligence technology acceptance in managerial accounting. Electronics, 11(14), 2256.

https://doi.org/10.3390/electronics11142256

Licensed

© 2026 Copyright by the Authors.

Licensed as an open access article using a CC BY 4.0 license.

Article Contents Author Danish Jameel1, * 1Central South University, Hunan, China Article History: Received: 08 April, 2026 Accepted: 17 June,

Article Contents Author Mirza Amin ul Haq1 , Shahzad Khalil2, * 1Department of Marketing, Ziauddin University, Karachi, Pakistan 2Department of

Article Contents Author Gilbert M. Talaue1, * Ishaq Kalanther1, Tomasa Gilberta D. Bitanga2 1Department of Business Administration, Jubail Industrial College,

Article Contents Author Asif Baig1, * 1Department of Business Administration, Jubail Industrial College, Jubail, Kingdom of Saudi Arabia Article History: Received:

Article Contents Author Huma Rasheed1, * , Iffat Saeed Channa2 , Samiya Kainat2 , Mohammad Affan Tahir2 1Herbal Biomedicine Inc,

Article Contents Author Murtuza Bhatti 1,2,* Imran Iqbal3 1Bath Spa University, London, United Kingdom; 2BPP University, London, United Kingdom; 3Commecs