Article Contents

Article ID: CM2621101019

Designing Last-Mile Trust: Behavioural Nudges and Community Agents for First-Use Intention/Experience

PDF

PDF

⬇ Downloads: 6

1Department of Business Management & Commerce, Desh Bhagat University, Mandi Gobindgarh, Punjab 147301, India

Received: 06 November, 2025

Accepted: 02 January, 2026

Revised: 31 December, 2025

Published: 11 February, 2026

Abstract:

Introduction: Last-mile adoption of digital finance often stalls at the first transaction because first-time users face uncertainty, cognitive load, and thin interpersonal trust. This study investigates whether behavioural nudges and perceived usefulness, combined with locally credible community agents, convert intention into first use of digital finance.

Methods: A community-based field survey (n = 250) was used for the data collection using a structured Likert-scale questionnaire measured on a 5-point scale. The participants were recruited using a random sampling approach, and the z-probability formula was applied to calculate the adequate sample size. The direct effects and moderating effects were analysed using PLS-SEM on SmartPLS.

Results/Findings: The findings of the study indicated the positive and statistically significant effect (β = 0.198, p = 0.010) of Behavioural Nudges, which implies that prompts that increase salience and simplified prompts are effective in transforming intention into first digital finance use. The direct effect of Community-Agent Trustworthiness is significant and strongly positive (β = 0.474, p < 0.001). Perceived Usefulness also exhibits a positive and significant direct relationship with first-use intention/experience (β = 0.073, p < 0.001). Community-Agent Trustworthiness plays a significant moderating role between Behavioural Nudges and first-use intention/experience (β = 0.021, p = 0.001). Likewise, Community-Agent Trustworthiness Interaction and Perceived Usefulness (β = 0.002, p = 0.003) have statistically significant results.

Conclusion/Implications: The findings suggest that the initial adoption of digital finance does not rely solely on the technological value or behavioural cues, but more importantly on locally based trust-based mechanisms. It is only by reinforcing behavioural nudges and perceived usefulness by trusted community agents that mitigate uncertainty at the point of initial implementation that behavioural nudges are effective. It underscores the importance of adoption policies that combine behavioural design with human relays, and proposes that scalable digital finance projects should focus on trust infrastructures in addition to technological innovation in order to obtain inclusive adoption.

JEL Codes: D91; C93; O33; O16; E42; G21.

Keywords: Behavioural nudges, perceived usefulness, trust, community agents, digital finance.

1. INTRODUCTION

The development of digital public infrastructure and fintech has significantly reduced the cost of financial transactions and added to the convenience for account holders to move their money. However, uptake by users with first-use intention and experience of digital finance in Malaysia still remains stuck at the so-called last mile, especially when it comes to onboarding or during the initial financial transaction (Gong, 2025; Safuri et al., 2024). In places where access is technically accessible, uncertainty, cognitive burden, and weak trust do not allow users to transform intention into action. Digital financial services have been growing at a rapid rate, with digital payments of RM21.5 billion in May 2025, an increase of 70% year-on-year, and e-wallet usage at 88% of adults in 2024, indicating a high proportion of consumers who have been receptive to the adoption of digital finance (Fintech News Malaysia, 2025). However, the situation with first-use intention/experience is not steady; that is, only 31% of Malaysians demonstrate great interest in digital banking, and the security aspect, the perception of complexity, and the lack of trust are identified as the primary barriers (Basar et al., 2022). As per (Jalil et al., 2021; and Zaghlol et al., 2021), it is further driven by ongoing cybersecurity threats and increasing cyber incidents, resulting in further distrust, especially among users who are not digitally savvy and people in rural areas, limiting inclusive usage.

Previous studies, such as (Ahmad & Yahaya, 2023; and Saif et al., 2022), define the future of the digital financial sector as well as the obstacles that suffocate adoption. The evidence in the cross-country context supports the view that affordability, proximity, and enabling institutions are predictors of digital finance usage adoption; large gaps between usage are still present despite the growth of access, as argued by (Allen et al., 2016). As per (Agarwal et al., 2024; and Che Nawi et al., 2022), integration of digital financial services, the behavioural frictions of perceived risk, and disorienting user experiences, which deactivate active use, are identified through reviews of digital financial services. Though much of this literature views trust as a broad notion and tends to measure it at the institutional level, or once adopted without differentiating institutional trust in banks, transactional trust in mobile money systems, and the situational trust that is needed to conduct a first digital transaction in the absence of a previous experience.

Evidence has always been pointing towards trust as a factor in the intention of using digital finance. Account ownership and usage are predicted by social trust and bank trust, and can work partially to compensate weak formal institutions, as argued by (Ghosh, 2021; and Xu, 2020). Users are hesitant to utilise the technology where they lack trust in the safety of data, the resolution of disputes, or the integrity of the agent; where the presence of trust increases, the number of women, rural households, and newly adopted smartphone users will use the technology. At the local level, proximate trust brokers can be community agents who are also identifiable as banking correspondents, mobile money agents, or accredited facilitators, as reflected by (Chamboko, 2024; and Neves et al., 2023). (Glavee-Geo et al., 2020; Shaikh et al., 2022) indicate that the credibility of agents and the quality of the services increase the empowerment and continuance, especially among the less financially empowered customers.

What is less explored is the more effective delivery of such nudges in the environment where users feel the presence of a trusted local intermediary. Although risk reduction is a motivating factor of the design logic of both nudges and agent support, moderation is not estimated in this paper. Rather, it examines the moderating effect of perceived community agent trustworthiness on the associational effect of behavioural nudges on First-use intention/experience. This paper is unique in that it jointly tests two pragmatic levers, behavioural nudges, which make the first digital financial use effective, and community agent trustworthiness, as perceived credibility, benevolence, and competence. Consequently, the objectives of the study are devised as:

1.1. Research Objectives

- Estimate the predictive relationship between behavioural nudges on first-use intention/experience.

- Examine the predictive relationship between the impact of perceived usefulness on first-use intention/experience of digital finance.

- Test whether community agent trustworthiness moderates the nudge and first-time intention experience relationship.

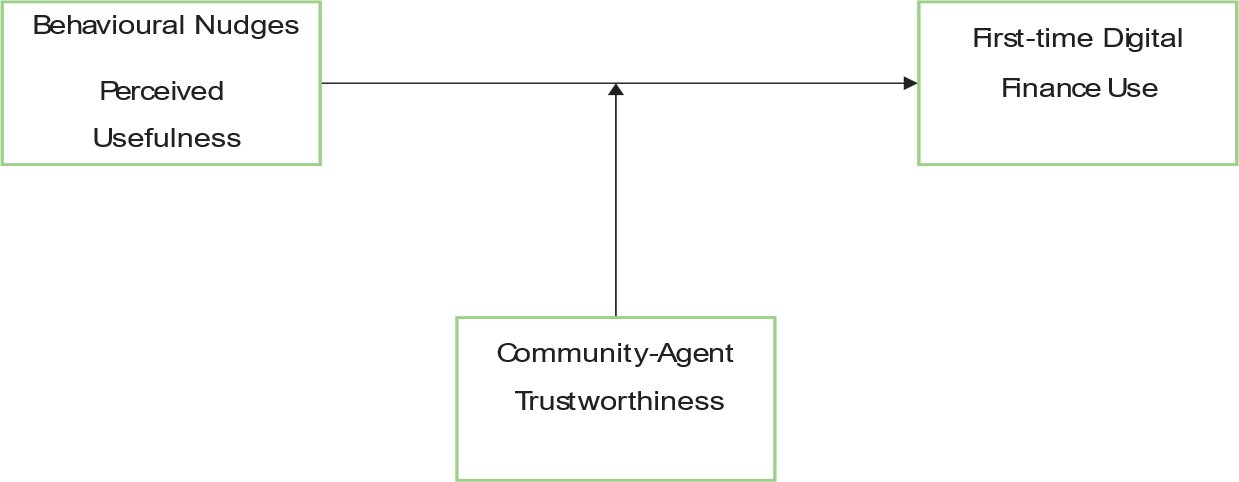

At first, the study makes a contextual contribution as a recombination where contextual plus first-use have been considered by assessing ways that established trust impacts the first-use intention and experience of digital finance in Malaysia, and provides empirical evidence on the relationship between factors behind first-time intention and experience of digital finance in Malaysia. Concerning theoretical contributions, this study has extended the TAM by incorporating the mechanisms of trust and behavioural intention at the first-use intention and experience, as opposed to signifying the weaknesses of the Technology Acceptance Model. The importance of perceived usefulness establishes the explanatory power of TAM, and the fact that the contextual and relational aspects are moderated by community-agent trustworthiness proves the role of contextual and relational factors in the practical condition of technology acceptance. The results, therefore, supplement, but do not refute, TAM by demonstrating that its fundamental constructs do not exist in the wider trust-based settings in emerging digital finance settings. Grounded on the identified research gaps, contributions, and purpose of the study, Fig. (1) represents the conceptual framework of the study.

Fig. (1). Conceptual and hypothesis model.

Source: Author’s design based on (Allen et al., 2016; Karlan et al., 2016; Xu, 2020).

2. Literature Review

2.1. Talent Last-Mile Trust Deficits in First-Use Intention/Experience of Digital Finance

The current literature is in agreement that trust is the core of digital finance adoption, although there is a difference in the way trust is theorised and to what extent it is directly connected to the initial decision points. Reconceptualising trust as a process instead of such a belief, (Krishna et al., 2025) portrayed the concept of trust as influenced by visible institutional commitments to cybersecurity. They demonstrate that the users of digital finance find trustworthiness based on institutional performance, responsiveness, and value alignment using a qualitative critical realist approach in India. This paper points out the situational development of trust in times of perceived vulnerability, which is directly related to the first use intention and experience.

(Ramli et al., 2021; and Mufarih et al., 2020), on the contrary, use Technology Acceptance Model (TAM) extensions to discuss the adoption of digital banking in Indonesia, incorporating trust as an intermediary or parallel attitudinal variable. According to (Ramli et al., 2021), perceived usefulness is the most predictive variable of intention, and trust has an indirect impact on intention via TAM variables. Nevertheless, they also note continually low real usage, which means that intentions do not always result in initial transactions. (Mufarih et al., 2020), on the contrary, consider perceived trust and perceived risk more significant than perceived usefulness or ease of use, meaning that issues associated with trust are predominant in the decision-making process in early-stage adoption situations.

These conflicting results reveal the drawbacks of the conventional uses of TAM. Although TAM is a good way to understand the evaluative beliefs on technology, it does not seem to be adequately fitting for the first-use hesitation based on the security uncertainty and the absence of an experiential point of reference. Both (Ramli et al., 2021; and Mufarih et al., 2020) use cross-sectional surveys and self-reported intention to make inferences, which restricts the ability to make inferences about behaviour at the first-use margin. None of the literature puts such an isolating spot on the moment of decision of the initial transaction and how trust is actively made during that point in time. Taken together, the literature indicates that last-mile trust deficit concerns are less due to usability limitations and rather due to unaddressed security and credibility issues during the initial use, which are one of the areas where current TAM-based and institutional analyses are empirically sparse.

2.2. Behavioural Nudges to Enhance Digital Finance Platforms Usage

Behavioural nudges have emerged as a low-cost approach to enhancing contact with digital finance platforms by overcoming psychological, not irrational, limitations, instead of structural limitations. Based on behavioural finance, (Aya et al., 2024) summarise the evidence that cognitive biases, including loss aversion, status quo bias, overconfidence, and judgment based on heuristics, can influence fintech adoption in a systematic way. Their review claims that resistance to unfamiliar technologies can be overcome by nudges such as social proof, along with salience cues and security framing. Although densely conceptualised, the study is very descriptive in nature, and it requires an empirical verification of the transformation of such nudges into actual platform use.

Empirical studies offer more divergent and context-specific evidence. (Talwar et al., 2020; and Chin et al., 2022) demonstrate that the adoption intentions and attitude toward fintech services can be enhanced through nudges presented through the digital interface, including simplified choice architecture and default options. Nevertheless, most of these studies are mainly based on survey-based studies and self-reported intentions, which restrict the evidence of first-use behaviour. In comparison, big-scale experimental data indicate that behavioural nudges have the potential to affect actual first-time intention and experience of using digital finance services. As demonstrated by (Jalil et al., 2021), reminders and framing interventions are highly effective in boosting savings behaviour, which makes salience and time-related factors a potent tool to overcome procrastination. Equally, (Fahad & Shahid, 2022) discovered that behavioural prompts are effective in promoting the digital payment adoption, especially among less experienced users.

More recent studies in experimental economics and psychology narrow down on these insights. (Chen et al., 2021) show that the exploitation of social norms and commitment devices can significantly transform economic decisions, whereas their impact can be influenced by the trust in a situation and perceived risk. The synthesis of evidence in (Chin et al., 2022) supports the idea that nudges are best applied in situations where the depth of decision-making is low and uncertainty is minimised, which the first-use intention/experience of digital finance does not usually have.

Combined, the literature indicates that though behavioural nudges increase the use of digital finance, their effect is not consistent or automatic. The discrete decision to use it first is not the focus of most of the studies, but is an intention or repeated behaviour. Besides, not many studies explicitly address the role of trust conditions in moderating the effectiveness, so it is not clear whether nudges are sufficient to predict first-time intention and experience of using digital finance. Based on these literature arguments, the following H1 of the study is formulated;

H1: Behavioural nudges increase first-use intention/experience of digital finance in the context of Malaysia.

2.3. Perceived Usefulness and First-Use Intention/Experience of Digital Finance

Perceived usefulness takes the centre stage in the Technology Acceptance Model (TAM), in which the users or consumers believe a technology will result in better performance of a task and provide tangible benefits, as argued by (Chamboko, 2024). Its applicability in the adoption of digital finance is always empirically supported, but significant differences are observed in terms of context, the type of user, and the level of use. (Ghani et al., 2022) prove that the perceived usefulness has a positive impact on digital banking effectiveness in Malaysian bank customers, which supports the instrumental logic of TAM. Their results indicate that users have an inclination to use digital banking to realise functional advantages, through efficiency and reliability. Nevertheless, the research analyzes the effectiveness among those users who are already existing users of one bank, which excludes the effectiveness in the context of the first-time intention and experience.

(Prastiawan et al., 2021) build upon TAM by adding social influence and attitude toward use and reveal that perceived usefulness has both direct and indirect impacts on the use of mobile banking among micro-entrepreneurs. In contrast to (Ghani et al., 2022), the given study captures the dynamics of early adoption, emphasising that attitudes influencing the adoption into usage are formed on the basis of usefulness perceptions. However, the moderation of attitude causes a distortion of the intention and experience of using digital finance for the first time, which is a weakness of the TAM-based models. Both studies applied cross-sectional surveys and self-reported use, which limits a causal conclusion and does not isolate an initial decision on the transaction. Neither discusses the interaction between perceived usefulness and trust or behavioural last-mile interventions. These gaps imply that, though perceived usefulness is a prerequisite, it is not sufficient to explain first-time digital finance use, and therefore, integrative models need to be incorporated to enumerate trust and behavioural nudges.

H2: There is a statistically significant effect of perceived usefulness on the first-use intention/experience of digital finance in the case of Malaysia.

2.4. Community Agents as a Moderator Between Last Mile Trust and First-Time Digital Finance Usage

The community agents, merchant agents, banking correspondents, and community facilitators are commonly defined as intermediaries that localise digital financial systems and minimise the uncertainty at the point of contact. It has been demonstrated that agents improve access and information frictions and that transaction activity is increased in places with higher numbers of agents (especially among low-income users), which suggests that agents reduce information and access costs, as suggested by (Chamboko et al., 2021; and Cull et al., 2018). Much of this literature, however, deals with aggregate utilisation or post-adoption behaviour instead of separately considering the first-use decision, where the lack of trust is greatest, and the educational experience is non-existent.

The analysis of agent features is done using studies that show relational aspects of the features that can be applied to first-time users. (Chamboko et al., 2021) show that identifying as an agent, gendering, and social network entrenchment influence the earlier interaction among women and marginalised groups. These results indicate that the agent’s trustworthiness is multidimensional, which includes the perceived competence, benevolence, and social alignment. But measurement is imprecise: it is common to assume the credibility of the agent based on the density, satisfaction, or retention, but not based on the perception of the user at the time of the first interaction.

This limitation gets strengthened by service quality research. (Twum et al., 2023) demonstrate that mobile money systems satisfaction and continuance are predicted by agent availability, security practices, responsiveness, and expertise. Although these features probably form early impressions, the research papers fail to separate the effect of agents to create an initial trial or to maintain usage after adoption. Ideologically, these gaps indicate a moderating position of the agents of the community. Instead of causality, agent credibility moderates the first-time intention and experience of the user to trust-building interventions. In particular, the work of trusted agents can magnify the influence of behavioural nudges because abstract promises can be transformed into credible and individualised advice at the point of the initial use, thus moderating the relationship between last-mile trust interventions and First-use intention/experience.

Even though community-agent trustworthiness has a strong direct effect on first-use intention and experience, its moderating effect is theoretical in nature. As unveiled by (Chamboko et al., 2021), trust moderates the conversion of behavioural nudges and perceived usefulness into action, especially in the face of high uncertainty, by alleviating cognitive barriers, instantiating claims of institutions, and giving reassurance. This has been in line with the relational and behavioural theories, which have proposed credible intermediaries to facilitate the expression of latent intentions into action. Consequently, despite overwhelming direct effects, moderation has the power to describe the conditional process in which trust increases the efficacy of adoption levers, thereby warranting its consideration as an essential interaction.

H3: Community agent trustworthiness moderates the effect of behavioural nudges and perceived usefulness on first-use intention/experience of digital finance in the case of Malaysia.

3. Materials and Methods

3.1. Research Design and Sampling

The instrument utilised in data collection is a five-point Likert-scale questionnaire that comprised three items that measured the four constructs of the study, which were comprised of Behavioural Nudges, perceived usefulness, Community Agent Trustworthiness, and Digital Finance Usage. The questionnaire focused on first-time users of digital finance and took between 15 and 20 minutes to complete.

The required sample size was determined using G*Power 3.1, which, as per (Kang, 2021), suggests finding the required size of a sample in PLS-SEM research assuming a medium effect size (f2 = 0.15), a significant value of 0.05, and a power of 0.80. This analysis showed that the minimum sample size is 200; thus, a target sample of 250 respondents was arrived at to increase the stability of the estimation proposed by (Freeman et al., 2013) as well. A non-probability convenience sampling method was used to collect data by means of professional contacts and social media. Out of these 700 people, 300 answered (response rate 43%). The valid response numbered 250 was obtained after the elimination of 50 questionnaires that lacked any data and outliers that satisfied the G*Power criterion. Although this method has a detrimental impact on statistical generalizability, it is suitable for theory testing and exploratory modelling in digital finance studies where formal sampling frames to access first-time users are limited, as recommended by (Iliyasu & Etikan, 2021). Furthermore, the risk of selection bias was also addressed by recruiting participants from different professional and social platforms, such as LinkedIn and Instagram, with experience of using digital finance applications and representing different demographic characteristics. To address the non-response, a difference in early (n = 30) and late (n = 30) respondents was examined, where no significant difference ruled out the issue of non-response bias, as suggested by (Jabkowski et al., 2025).

Though the current research targets first-use intention and the experience with using digital finance, first-time users cannot be grouped with low education or digital illiteracy, because many adults put off the first use of digital finance applications because they have access and basic digital skills, but are reluctant to use them because of trust concerns, perceived risk and lack of knowledge of the effect such applications would have. The recruitment through professional and social media platforms, therefore, facilitated access to the late adopters who had not been conducting digital finance transactions before. The identified age and education cohort thus represents trust-constrained first-time users and not digitally marginalised groups. Such framing positions the sample in line with the theoretical subject of the study, which is trust and the mechanics of behaviour that form first-use decisions.

3.2. Statistical Methods

The analysis of data was carried out in two phases so that rigour and robustness could be guaranteed. They measured the constructs by first determining the reliability and validity of the measurement model. To verify the internal consistency and convergent validity, Cronbach’s alpha, composite reliability (CR), and average variance extracted (AVE) were computed in accordance with the recommendations of (Mohd Dzin & Lay, 2021). Constructs having a Cronbach alpha and CR equal or exceeding 0.7 and AVE equal or exceeding 0.5 were deemed to be acceptable to achieve psychometric standards on the measurement model suggested by (Cheung et al., 2024). Second, aligned with (Gorai et al., 2024), the structural model was validated with the help of Partial Least Squares Structural Equation Modelling (PLS-SEM) in SmartPLS, which is better suited for predictive modelling with complex models and small samples. The effect of Perceived Usefulness and Behavioural Nudges on Digital Finance Usage was directly investigated, and the moderating influence of Community Agent Trustworthiness on it was also investigated.

Since self-report survey data were used for all the constructs of the study, the common method variance (CMV) issue had to be addressed. Procedural remedies were implemented based on the recommendations of (Mohd Dzin & Lay, 2021), which entail: assured anonymity, psychological separation of constructs, and clear and concise items, to minimise apprehension of evaluation. As suggested by (Iliyasu & Etikan, 2021), CMV was estimated statistically by Harman’s single-factor test, which indicated that no one factor explained most of the variance, which means that CMV would not bias the results. All these procedural and statistical controls increase the degree of confidence that relationships that are observed are an expression of substantive effects, and not a manifestation of common method bias.

3.3. Ethics & Approvals

All procedures comply with the Declaration of Helsinki and all relevant institutional review board (IRB) or ethics committees’ standards, specifically prior protocol reviews, community entry approvals, and enumerators certified in protecting human subjects. All participation is voluntary, and respondents are asked for their informed consent using an electronic tool; respondents have the right to bypass any question(s), leave the survey at any point, and will incur no consequences. Personal identifiable information is separated from the respondent’s survey data; device-level encryption, limited access to the data collected, and de-identified analytic files will provide confidentiality for all respondents. Due to the low-risk nature of this study (the respondents will be briefly nudged and asked to complete a short survey, no deception will be used in the study, and the respondents will receive a small amount of money as an approved token of appreciation by local norms).

4. Results

4.1. Descriptive Statistics

Table 1 contains socio-demographic information regarding respondents’ ages. Respondents appear to be concentrated in early to mid-working age, with moderate variability. The results also indicate that the sample includes 24.8% of the sample population who held primary education or less, 41.6% held secondary education, 32% were college and university graduates, and 1.6% held other qualifications. Moreover, 41.2% of the total population represented the rural population, 26% semi-urban, and 32.8% were from Urban areas. Lastly, most of the participants, that is, 31.6% and 33.6% earn less than 15k and between 15-30k, respectively.

Table 1. Demographic characteristics.

| Variable | Category | Count | Percent |

| Age | M = 40.92, SD = 13.41 | ||

| Gender | Female | 122 | 48.8 |

| Male | 116 | 46.4 | |

| Non-binary | 9 | 3.6 | |

| Prefer not to say | 3 | 1.2 | |

| Education | Primary or less | 62 | 24.8 |

| Secondary | 104 | 41.6 | |

| College/University | 80 | 32 | |

| Other | 4 | 1.6 | |

| Locations | Rural | 103 | 41.2 |

| Semi-urban | 65 | 26 | |

| Urban | 82 | 32.8 | |

| Monthly Household Income (local currency) | <15k | 79 | 31.6 |

| 15–30k | 84 | 33.6 | |

| 30–60k | 62 | 24.8 | |

| >60k | 25 | 10 | |

4.2. Measurement Model-Confirmatory Factor Analysis

The measurement model of the study is tested for reliability and validity using confirmatory factor analysis, which comprises Cronbach’s Alpha, Composite Reliability, and Convergent Validity using Average Variance Extracted. The results are specified in Table 2.

Table 2. Validity and reliability.

| Latent Variables | Indicators | Factor Loadings | Cronbach’s Alpha | Composite Reliability (rho_a) | Average Variance Extracted (AVE) |

| Behavioural Nudges | BU1 | 0.872 | 0.822 | 0.831 | 0.737 |

| BU2 | 0.873 | ||||

| BU3 | 0.829 | ||||

| Community-Agent Trustworthiness | CAT1 | 0.880 | 0.880 | 0.884 | 0.807 |

| CAT2 | 0.930 | ||||

| CAT3 | 0.884 | ||||

| First-use intention/experience | FUI1 | 0.915 | 0.910 | 0.910 | 0.847 |

| FUI2 | 0.935 | ||||

| FUI3 | 0.911 | ||||

| Perceived Usefulness | PU1 | 0.816 | 0.800 | 0.810 | 0.715 |

| PU2 | 0.903 | ||||

| PU3 | 0.815 |

The results specified in Table 2 signify that all the constructs in the measurement model show high factor loading between (0.815-0.935). On the other hand, with respect to reliability, almost all the constructs in the measurement model show how reliability with Cronbach’s Alpha and Composite Reliability is well above the threshold of 0.7 (α > 7). In the case of convergent validity, all the constructs are found to depict high convergent validity with AVE values surpassing the threshold of 0.5.

4.3. Discriminant Validity

The discriminant validity test using the HTMT ratio with a standard value of 0.85 allows for examining the separability and distinctiveness among variables, which also determines whether there is a presence of conceptual overlapping among constructs suggested by (Afthanorhan et al., 2021). The results are shown in Table 3.

Table 3. Discriminant validity.

| Behavioural Nudges | Community-Agent Trustworthiness | First-time Digital Finance Use | |

| Community-Agent Trustworthiness | 0.694 | ||

| First-use intention/experience | 0.590 | 0.696 | |

| Perceived Usefulness | 0.531 | 0.414 | 0.378 |

The results specified in Table 3 show that the values of the HTMT ratio are below the threshold of 0.85, which indicates that the variables are conceptually separable and distinctive from each other, with a sign of overlapping.

4.4. Path Coefficient Analysis

The results of the path coefficient analysis in Table 4 suggest significant direct effects on the First-use intention/experience. The positive and statistically significant effect (β = 0.198, p = 0.010) of Behavioural Nudges implies that prompts that increase salience and simplified prompts are effective in transforming intention into first-use intention/experience of using digital finance. The direct effect of Community-Agent Trustworthiness is significant and strongly positive (β = 0.474, p < 0.000), which means that perceived agent credibility, competence, and benevolence dominate the first-use intention/experience of using digital finance in the state of uncertainty. Perceived Usefulness also exhibits a positive and significant direct relationship with first-use intention/experience of digital finance (β = 0.073, p < 0.027), which supports expectations of TAM based on the fact that functional value perceptions have an independent effect on adoption, though the strength thereof is not as strong.

Table 4. Path analysis.

| Path Coefficients | T-statistics (|O/STDEV|) | P-values | |

| Behavioural Nudges -> First-use intention/experience | 0.198 | 2.576 | 0.010 |

| Community-Agent Trustworthiness -> First-use intention/experience | 0.474 | 6.419 | 0.000 |

| Community-Agent Trustworthiness x Behavioural Nudges -> First-use intention/experience | 0.021 | 2.334 | 0.024 |

| Community-Agent Trustworthiness x Perceived Usefulness -> First-use intention/experience | 0.002 | 3.234 | 0.003 |

| Perceived Usefulness -> First-use intention/experience | 0.073 | 2.219 | 0.027 |

Using moderation analysis, it is found that Community-Agent Trustworthiness plays a significant moderating role between Behavioural Nudges and first-use intention/experience (β = 0.021, p = 0.024). This result points to a finding that nudges are more effective when administered within a setting where the perceived agent trustworthiness is high, which in turn reinforces the argument that trusted intermediaries increase behavioural interventions. Likewise, Community-Agent Trustworthiness Interaction and Perceived Usefulness (β = 0.002, p = 0.003) have statistically significant results, which suggest that the perceptions of usefulness are more apt to action in case they are supported by trusted agents. In general, the findings highlight that nudges and usefulness are important factors, but the key facilitating factor in the use of digital finance by first-use intention/experience of using digital finance is the element of trust, reflected by community agents.

5. Discussion

The results confirm the H1 hypothesis and prove that behavioural nudges positively and significantly influence First-use intention/experience in Malaysia. The outcome is consistent with the previous behavioural finance and adoption literature, where (Venkatesh et al., 2012) have found reminders, salience cues, and simplified choice structures to overcome procrastination and cognitive overload. In line with (Aya et al., 2024), the findings validate the fact that making decisions without sufficient rationality is a critical aspect of fintech usage, especially when the potential customers are uncertain. The effect size in this study is, however, small compared to some of the experimental results in developed markets, which might indicate that there are contextual limitations.

This can be attributed to cultural and industrial factors. In Malaysia, the adoption intention and experience of digital finance have been growing at a high rate, although the issues of trust and perceived cybersecurity threats are still relevant, especially with first-time users and rural areas, as suggested by (Oliveira et al., 2016). Trying to compare the nudges to situations when they are conducted in a high-trust institutional background, Malaysian digital finance users might need more assurance than behavioural prompts in their case. It corresponds to the idea proposed by (Karaca-Mandic et al., 2012), according to which nudges are less efficient in high-uncertainty settings, unless they are supported by mechanisms of trust.

These findings are also related to TAM theory, where behavioural nudges do not substitute substantive evaluative beliefs, but instead act concomitantly with them by minimising decision inertia instead of changing the perceived utility directly. The results suggest that nudges are created to deal with the intention-action gap and not with value evaluation. In practice, this highlights the significance of instilling nudges at decisive points of onboarding and their shortcomings in cases of the lack of trust. Therefore, the effect of behavioural nudges is valid, but it depends on the general conditions of trust in new digital finance ecosystems and their usage.

The findings support H2, and the hypothesis has been confirmed that perceived usefulness is an important factor in the First-use intention/experience in Malaysia. This is in agreement with the underlying Technology Acceptance Model that places the perceived usefulness as one of the key determinants of technology adoption, suggested by (Grohmann et al., 2018; and Neves et al., 2023) as well. The role of functional value in adoption decisions has been supported, so there is empirical alignment with (Ghani et al., 2022), who show that perceived usefulness increases digital banking effectiveness in Malaysia.

Nevertheless, the comparatively low effect size in this study is opposed to TAM-related results in developed and corporate banking settings, assuming that the perceived usefulness frequently prevails in the adoption process (Prastiawan et al., 2021). This variation is a contextual difference in the first-time use intention and experience. In the case of the Malaysian first-time user, especially those who have not been exposed to detailed information, usefulness might not be enough to prompt them to use digital finance applications when they are also not sure about the safety and reliability of the security, as well as the procedural fairness.

The Malaysian digital finance users are culturally in a hybrid of financial ecosystem, in which cash and informal systems co-exist with digital operations. This has led to the fact that usefulness is no longer judged based purely on efficiency, but also based on the perceived risks and trustworthiness, which is in line with the arguments of (Agarwal et al., 2024) also. This substantiates arguments against TAM that call to extend its context in new markets. Although perceived usefulness creates a baseline motivation, this does not rule out the first-use hesitation.

In theory, the results confirm the applicability of TAM but indicate its weaknesses in the explanation of first-use behaviour in the face of uncertainty. In practice, value propositions should be supported by trust-building mechanisms by digital finance providers in order to make usefulness perceptions become actionable. This finding indicates that usefulness is required but not sufficient in the first-time adoption of digital finance in Malaysia.

The results are consistent with H3 and led to its acceptance, which illustrates that the trustworthiness of community agents produces a high moderating effect on the impact of behavioural nudges and perceived usefulness on first-use intention/experience of using digital finance applications. This finding builds upon previous studies by having a moderating influence as opposed to a direct or moderating relationship. Although other researchers focus on the role of agents in continuance and satisfaction Shaikh et al., 2022; Twum et al., 2023), in this paper, agent trustworthiness determines user reaction to interventions when making the first-use intentions to use digital finance.

This is in agreement with (Chamboko et al., 2021), who emphasise the role of agent identity and social embeddedness in early engagement but go an extra mile to show that trusted agents maximise the impact of both nudges and perceived usefulness. Such an interaction effect is in opposition to the results in high-trust digital economies, in which only an institutional guarantee might be necessary. The interpersonal credibility in the interpretation of abstract systems claims into constructive confidence is important in the mixed-trust environment of Malaysia. Theoretically, the findings fill a major gap in the TAM through the contextual moderator that determines the belief-behaviour translation. Instead of changing the perceived usefulness directly, trusted agents decrease situational uncertainty, which permits users to respond to current beliefs and prompts.

This substantiates criticism that TAM is too weak in its relational and social trust processes in emerging markets. In practice, the results suggest that investments into agent training, credibility signalling, and local trust-building can play a significant role in terms of their effectiveness in digital adoption strategies. Community agents do not simply become service providers, but they are essential facilitators of last-mile trust in the First-use intention/experience. In addition, the findings do not nullify technology-based adoption paradigms but point to their situational contingency. Although perceived usefulness works in the theoreticised form, its functionality is determined by trust conditions when it is first used. This implies that the technology-based explanations can still hold, but will be incomplete when used to explain first-use intention and experience in high-uncertainty settings. Trust and behavioural design are thus a considered complementary layer that augments but do not substitute the already developed technology adoption frameworks.

Community-agent trustworthiness has a direct impact on the first-use intention, but its moderating aspect brings forward the vital conditional process. High trust reinforces the effects of behavioural nudges so that reminders, default options, and simplified prompts are viewed as authentic and viable. This implies that nudges are ineffective in high-uncertainty situations on their own, and trust is a facilitating factor, which transforms latent intention into actual interaction. This is conceptually in line with behavioural and relational trust models, which contribute to the argument that moderation reflects the situational enhancement of interventions that cannot be accounted for by direct effects suggested by (Twum et al., 2023). Similarly, trust moderates the impact of the usefulness perceived on first-use intention and experience, which means that the usefulness of the functionality is not necessarily enough to evoke action.

Increased perceptions of usefulness through the validity of agents leads to users reinforcing the perceptions of usefulness, reducing uncertainty, and facilitating the shift of evaluation to action. This highlights the fact that moderation is a characteristic of adoption that is conditional in the new digital finance environments. Theoretically, it shows that trust allows the operationalization of TAM constructs even in the real-world situation of uncertainty in operation, justifying the theoretical decision to give primary importance to moderation in the situation where the direct effects of trust are prevalent.

Conclusion

This study has shown that closing the first-use intention/experience gap in digital finance not only needs enhancements in access or interface design, but also must be carefully engineered to build trust at the last mile. The results negated the purely technology-based usage paradigms by demonstrating that behavioural nudges and perceived usefulness are not adequate in their own right in a high uncertainty financial environment like Malaysia. Rather, trust as represented by the community agents develops as a determining enabling condition that transforms intention into action. The study does not present an independent design rule, but extends to the existing adoption models by combining behavioural nudges and trusted human intermediaries. The contribution is in the empirical demonstration of the interaction effect of these factors with the constructs of TAM in making a first-use decision. The study, by placing the technology acceptance in the framework of relational trust, provides the contextualized design consideration to digital finance onboarding, as opposed to an alternative to the traditional theoretical frameworks. The findings indicate that the inclusive digital finance approaches should combine both behavioural design and locally based trust systems. Digital finance is in danger of enhancing exclusion instead of technology in the absence of valid human intermediaries.

Limitations and Future Directions

This research has a certain limitation, which provides guidance for future research. First, the cross-sectional research design limits causal inference and fails to measure the changes in trust and usage over time; a longitudinal or experimental research design can enhance causal arguments. Second, dependence on self-reported instruments of First-use intention/experience can also create recall or social desirability bias; subsequent research can use transaction-level or platform-authenticated data. Third, emphasis on Malaysia restricts external validity to other institutional settings; a comparative cross-country study would be more effective at ensuring external validity. Further investigation is also needed in future studies on other moderators, including regulatory trust or the features of a platform design that can further unpack the dynamics of last-mile adoption.

Policy Implications

The results provide valuable policy suggestions to the regulators, financial institutions, and fintech providers. Policy makers must go beyond the expansion of access and directly include trust-building instruments in national policy on digital finance, especially through the empowerment and certification of community agent networks. The regulators may increase trust through transparent cybersecurity policies and observable consumer protection systems. Financiers and technological companies in fintech need to develop adoption strategies that combine behavioural nudges with trusted human interfaces, particularly in the onboarding and initial transactions. The effect of digital inclusion initiatives can be enhanced by investing in agent training, signalling credibility, and settling grievances. In general, there are higher chances of success in inclusive and sustainable digital finance adoption when policies are congruent with behavioural design and locally-based trust infrastructures.

LIST OF ABBREVIATIONS

TAM = Technology Acceptance Model

CR = Composite Reliability

AVE = Average Variance Extracted

CMV = Common Method Variance

PLS-SEM = Partial Least Squares Structural Equation Modelling

Authors’ Contributions

G.P.K. contributed to the design and implementation of the study. R.S. contributed to the analysis of the results and the writing of the manuscript.

Ethical Approval

All procedures comply with the Declaration of Helsinki and all relevant institutional review board (IRB) or ethics committees’ standards, specifically prior protocol reviews, community entry approvals, and enumerators certified in protecting human subjects. All participation is voluntary, and respondents are asked for their informed consent using an electronic tool.

AVAILABILITY OF DATA AND MATERIALS

De-identified survey dataset, codebook, and analysis scripts available from the corresponding author upon reasonable request, subject to ethics approvals and participant confidentiality safeguards governing data sharing.

Funding

None.

Conflict of interest

The authors declare no conflicts of interest.

ACKNOWLEDGEMENTS

Grateful to participating communities, enumerators, and local agents for cooperation; appreciation to anonymous reviewers for methodological comments.

References

Afthanorhan, A., Ghazali, P. L., & Rashid, N. (2021). Discriminant validity: A comparison of CBSEM and consistent PLS using Fornell & Larcker and HTMT approaches. In Journal of Physics: Conference Series (Vol. 1874, No. 1, p. 012085). IOP Publishing. DOI:10.1088/1742-6596/1874/1/012085

Agarwal, S., Ghosh, P., Li, J., & Ruan, T. (2024). Digital payments and consumption: Evidence from the 2016 demonetization in India. The Review of Financial Studies, 37(8), 2550–2585. https://doi.org/10.1093/rfs/hhae005

Agarwal, A., & Assenova, V. A. (2024). Mobile money as a stepping stone to financial inclusion: How digital data enable credit access. Organization Science, 35(3), 769–787. https://doi.org/10.1287/orsc.2022.16562

Ahmad, K., & Yahaya, M. H. (2023). Islamic social financing and efficient zakat distribution: impact of fintech adoption among the asnaf in Malaysia. Journal of Islamic Marketing, 14(9), 2253-2284. DOI: 10.1108/JIMA-04-2021-0102

Allen, F., Demirgüç-Kunt, A., Klapper, L., & Martínez Pería, M. S. (2016). The foundations of financial inclusion: Understanding ownership and use of formal accounts. Journal of Financial Intermediation, 27, 1–30. https://doi.org/10.1016/j.jfi.2015.12.003

Aya, M., Abdessalam, N. W., & Houda, B. (2024). From Theory to Practice: Behavioral Finance’s Influence on Fintech Innovation and Regulatory Frameworks. Int. J. Econ. Stud. Manag, 4(5). DOI:10.5281/zenodo.14202583

Basar, S. A., Zain, N. N. M., Tamsir, F., Rahman, A. R. A., Ibrahim, N. A., & Poniran, H. (2022). How digital financial literacy affects i-fintech adoption among bumiputera smes in selangor, Malaysia. International Journal of Accounting, Finance and Business, 7(43), 587-601. DOI:10.55573/IJAFB.074343

Chamboko, R. (2024). Digital financial services adoption: A retrospective time-to-event analysis approach. Financial Innovation, 10, Article 46. https://doi.org/10.1186/s40854-023-00568-1

Chamboko, R., Cull, R., Giné, X., Heitmann, S., Reitzug, F., & Van der Westhuizen, M. (2021). The role of gender in agent banking: Evidence from the Democratic Republic of Congo. World Development, 146, Article 105551. https://doi.org/10.1016/j.worlddev.2021.105551

Che Nawi, N., Mamun, A. A., Hayat, N., & Seduram, L. (2022). Promoting sustainable financial services through the adoption of eWallet among Malaysian working adults. Sage Open, 12(1), 21582440211071107. https://doi.org/10.1177/21582440211071107

Cheung, G. W., Cooper-Thomas, H. D., Lau, R. S., & Wang, L. C. (2024). Reporting reliability, convergent and discriminant validity with structural equation modeling: A review and best-practice recommendations. Asia pacific journal of management, 41(2), 745-783. https://doi.org/10.1007/s10490-023-09871-y

Chin, A. G., Harris, M. A., & Brookshire, R. (2022). An empirical investigation of intent to adopt mobile payment systems using a trust-based extended valence framework. Information Systems Frontiers, 24, 329–347. https://doi.org/10.1007/s10796-020-10080-x

Cull, R., Giné, X., Harten, S., Heitmann, S., & Rusu, A. B. (2018). Agent banking in a highly under-developed financial sector: Evidence from the DRC. World Development, 107, 54–74. https://doi.org/10.1016/j.worlddev.2018.02.019

Fahad, M. S., & Shahid, M. (2022). Exploring the determinants of adoption of Unified Payment Interface (UPI) in India. Digital Business, 2(2), Article 100040. https://doi.org/10.1016/j.digbus.2022.100040

Fintech News Malaysia. (2025). Malaysia Fintech Report 2024: Will Digital Banks Usher in a New Era of Banking? Retrieved from https://fintechnews.my/46894/malaysia/fintech-malaysia-report-2024/

Freeman, G., Cowling, B. J., & Schooling, C. M. (2013). Power and sample size calculations for Mendelian randomization studies using one genetic instrument. International journal of epidemiology, 42(4), 1157-1163. https://doi.org/10.1093/ije/dyt110

Ghani, E. K., Ali, M. M., Musa, M. N. R., & Omonov, A. A. (2022). The effect of perceived usefulness, reliability, and COVID-19 pandemic on digital banking effectiveness: Analysis using technology acceptance model. Sustainability, 14(18), 11248. https://doi.org/10.3390/su141811248

Ghosh, S. (2021). How important is trust in driving financial inclusion? Journal of Behavioral and Experimental Finance, 32, Article 100510. https://doi.org/10.1016/j.jbef.2021.100510

Glavee-Geo, R., Shaikh, A. A., Hinson, R. E., & Karjaluoto, H. (2020). Mobile money usage and continuance intention among micro-enterprises: The mediating role of agent credibility. Journal of Systems and Information Technology, 22(4), 97–117. https://doi.org/10.1108/JSIT-03-2019-0062

Gong, D. R. (2025). Bridging Borders I: Malaysia’s Digital Payments Growth. Retrieved from https://www.krinstitute.org/publications/bridging-borders-i-malaysias-digital-payments-growth

Gorai, J., Kumar, A., & Angadi, G. R. (2024). Smart PLS-SEM modeling: Developing an administrators’ perception and attitude scale for apprenticeship programme. Multidisciplinary Science Journal, 6(12), 2024260-2024260. DOI:10.31893/multiscience.2024260

Grohmann, A., Klühs, T., & Menkhoff, L. (2018). Does financial literacy improve financial inclusion? World Development, 111, 84–96. https://doi.org/10.1016/j.worlddev.2018.06.020

Iliyasu, R., & Etikan, I. (2021). Comparison of quota sampling and stratified random sampling. Biom. Biostat. Int. J. Rev, 10(1), 24-27. DOI:10.15406/bbij.2021.10.00326

Jabkowski, P., Kohler, U., & Kołczyńska, M. (2025). Against All Odds: On the Robustness of Probability Samples Against Decreases in Response Rates. In Survey Research Methods (Vol. 19, No. 1, pp. 83-104). https://doi.org/10.18148/srm/2025.v19i1.8475

Jalil, M. F. (2021). Microfinance towards micro-enterprises development in rural Malaysia through digital finance. Discover sustainability, 2(1), 55. https://doi.org/10.1007/s43621-021-00066-3

Kang, H. (2021). Sample size determination and power analysis using the G* Power software. Journal of educational evaluation for health professions, 18. https://doi.org/10.3352/jeehp.2021.18.17

Karaca-Mandic, P., Norton, E. C., & Dowd, B. (2012). Interaction terms in nonlinear models. Health Services Research, 47(1, Pt. 1), 255–274. https://doi.org/10.1111/j.1475-6773.2011.01308.x

Karlan, D., McConnell, M., Mullainathan, S., & Zinman, J. (2016). Getting to the top of mind: How reminders increase saving. Management Science, 62(12), 3393–3411. https://doi.org/10.1287/mnsc.2015.2296

Krishna, B., Krishnan, S., & Sebastian, M. P. (2025). Understanding the process of building institutional trust among digital payment users through national cybersecurity commitment trustworthiness cues: a critical realist perspective. Information Technology & People, 38(2), 714-756. DOI:10.1108/ITP-05-2023-0434

Mohd Dzin, N. H., & Lay, Y. F. (2021). Validity and reliability of adapted self-efficacy scales in Malaysian context using PLS-SEM approach. Education Sciences, 11(11), 676. https://doi.org/10.3390/educsci11110676

Mufarih, M., Jayadi, R., & Sugandi, Y. (2020). Factors influencing customers to use digital banking application in Yogyakarta, Indonesia. Journal of Asian Finance, Economics and Business, 7(10), 897-908. DOI:10.13106/jafeb.2020.vol7.no10.897

Neves, A., Dias, A., & Correia, A. (2023). Adoption and use of digital financial services: A meta-analysis of barriers and facilitators. International Journal of Information Management Data Insights, 3(2), Article 100201. https://doi.org/10.1016/j.jjimei.2023.100201

Oliveira, T., Thomas, M., Baptista, G., & Campos, F. (2016). Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Computers in Human Behavior, 61, 404–414. https://doi.org/10.1016/j.chb.2016.03.030

Prastiawan, D. I., Aisjah, S., & Rofiaty, R. (2021). The effect of perceived usefulness, perceived ease of use, and social influence on the use of mobile banking through the mediation of attitude toward use. APMBA (Asia Pacific Management and Business Application), 9(3), 243-260. DOI:10.21776/ub.apmba.2021.009.03.4

Ramli, Y., Harwani, Y., Soelton, M., Hariani, S., Usman, F., & Rohman, F. (2021). The implication of trust that influences customers’ intention to use mobile banking. The Journal of Asian Finance, Economics and Business, 8(1), 353-361. DOI:10.13106/jafeb.2021.vol8.no1.353

Safuri, N. H., Sing, R. D. R., & Sing, K. K. (2024). Key Drivers of Gen Z’s Digital Banking Adoption in Malaysia: The Roles of Relative Advantage, Trust, and Perceived Value as a Mediator. Retrieved from https://hrmars.com/ijarbss/article/view/24237/Key-Drivers-of-Gen-Zs-Digital-Banking-Adoption-in-Malaysia-The-Roles-of-Relative-Advantage-Trust-and-Perceived-Value-as-a-Mediator

Saif, M. A., Hussin, N., Husin, M. M., Alwadain, A., & Chakraborty, A. (2022). Determinants of the intention to adopt digital-only banks in Malaysia: The extension of environmental concern. Sustainability, 14(17), 11043. https://doi.org/10.3390/su141711043

Shaikh, A. A., Glavee-Geo, R., Hinson, R. E., & Karjaluoto, H. (2022). Mobile money as a driver of digital financial inclusion. Technological Forecasting & Social Change, 186, Article 122158. https://doi.org/10.1016/j.techfore.2022.122158

Talwar, S., Dhir, A., Khalil, A., Mohan, G., & Islam, A. K. M. N. (2020). Point of adoption and beyond: Initial trust and mobile-payment continuation intention. Journal of Retailing and Consumer Services, 54, Article 102086. https://doi.org/10.1016/j.jretconser.2020.102086

Twum, K. K., Kosiba, J. P. B., Hinson, R. E., Gabrah, A. Y. B., & Assabil, E. N. (2023). Determining mobile money service customer satisfaction and continuance usage through service quality. Journal of Financial Services Marketing, 28(1), 30–42. https://doi.org/10.1057/s41264-021-00138-5

Venkatesh, V., Thong, J. Y. L., & Xu, X. (2012). Consumer acceptance and use of information technology: Extending UTAUT. MIS Quarterly, 36(1), 157–178. https://doi.org/10.2307/41410412

Xu, Y. (2020). Trust and financial inclusion: A cross-country study. Finance Research Letters, 35, Article 101310. https://doi.org/10.1016/j.frl.2019.101310

Zaghlol, A. K., Ramdhan, N. A., & Othman, N. (2021). The Nexus between Fintech Adoption and Financial Development in Malaysia: An Overview. Global Business & Management Research, 13(4): 365-375. https://www.gbmrjournal.com/pdf/v13n4/V13N4-30.pdf

Licensed

© 2026 Copyright by the Authors.

Licensed as an open access article using a CC BY 4.0 license.

Article Contents Author G. Prasanna Kumar1, * , Rajni Saluja1 1Department of Business Management & Commerce, Desh Bhagat University, Mandi

Article Contents Author Yazeed Alsuhaibany1, * 1College of Business-Al Khobar, Al Yamamah University, Saudi Arabia Article History: Received: 03 September,

Article Contents Author Muhammad Arslan Sarwar1, * Maria Malik2 1Department of Management Sciences, University of Gujrat, Gujrat, Pakistan; 2COMSATS

Article Contents Author Tarig Eltayeb1, * 1College of Business Administration, Imam Abdulrahman Bin Faisal University, Dammam, Saudi Arabia Article History:

Article Contents Author Kuon Keong Lock1, * and Razali Yaakob1 1Faculty of Computer Science and Information Technology, Universiti Putra Malaysia,

Article Contents Author Shabir Ahmad1, * 1College of Business, Al Yamamah University, Al Khobar, Kingdom of Saudi Arabia Article History: